‘Tis the Season… to Test for Radon

Radon gas isn’t a new issue for REALTORS®, but during this time of the year it gains importance as fall and winter are the ideal seasons to test for radon.

Understanding and helping mitigate radon risks is more than just a professional responsibility for REALTORS®. It's also an opportunity to provide clients with valuable information to help them make informed decisions.

There are many resources available to help support REALTORS® in building knowledge and awareness on radon, including an updated and accredited self-paced professional development course, BCFSA’s Radon Checklists for Buyers' Agents, Sellers' Agents, and Property Managers, a Radon FAQ and Testing Checklist, and some other online resources to incorporate into their practice.

Radon: Frequently Asked Questions and Checklists

Get a basic understanding of what radon is and how can you protect consumers in our blog, REALTORS® and Radon: Protecting Buyers and Sellers.

BCREA has also created a FAQ document on Radon with the support of Dr. Noah Quastel from the BC Lung Foundation. The document addresses common questions and provides external resources on the topic, including:

- what is radon;

- where radon is found in BC;

- which kind of homes need to be tested;

- and more.

And as a joint effort with the BC Lung Foundation and the Canadian National Radon Proficiency Program (C-NRPP), BCREA has designed a checklist for REALTORS® and the public to help ensure they follow the correct procedures in testing for radon.

Also, BCFSA provides guidance to help discuss the importance of radon with clients depending on the side of the transaction you’re in. See the checklists below:

- Radon Checklist for Sellers’ Agents

- Radon Checklist for Buyers’ Agents

- Radon Checklist for Rental Property Managers

Learn More About Radon and Your Responsibilities as a REALTOR®

Radon is an important consideration when buying a home. REALTORS® are expected to demonstrate competency and show skills when providing real estate services to their clients. Having knowledge about environmental conditions and signs of alert can help ensure you are taking the right steps to provide an exceptional experience.

BCREA has created a Radon for REALTORS® course, in which REALTORS® can deepen their understanding of radon and how it relates to the real estate transaction. By the end of this course, learners will be able to:

- understand and identify how radon enters a dwelling,

- know what influences radon levels,

- recognize the effects of radon on human health,

- understand Canada’s radon awareness initiatives,

- identify applicable laws and emergent policies on radon in BC and,

- much more

Demonstrate Your Radon Knowledge and You Could WIN!

In the spirit of inspiring and supporting REALTORS® to educate themselves about radon, BCREA is holding a contest. All you have to do is take and submit a short quiz demonstrating your radon knowledge, and you could win one of five lüft® Long-term Radon & Indoor Air Quality Monitors.

Deadline to complete: Friday, November 28, 2025, at 5 pm PT

Join the BC Lung Workshop: Radon: Collaboration for Healthy Communities

The BC Lung Foundation is hosting its annual virtual workshop to discuss the various actions individuals, families, researchers, communities, and government can do to address and prevent radon.

This webinar is eligible for two self-directed Professional Development hours.

Date: Tuesday, November 25, 2025

Time: 10 am to 11:30 am PT

“Limited Dual Agency Or No Agency,” There Is A Different #446

A recent case illustrates the pitfalls awaiting brokerages and REALTORS® when choosing to act as a limited dual agent.1

A couple engaged a brokerage and REALTOR® to assist them in the purchase of a house (the Grandview property). The Contract of Purchase and Sale for the Grandview property was subject to the sale of their existing house (the Carter property). The Contract of Purchase and Sale also contained a clause enabling the seller to require the couple to remove all of the subjects in the event the seller received another bona fide offer. After the acceptance of their conditional offer to purchase, the couple listed the Carter property with the same brokerage and REALTOR® that represented them in the acquisition of the Grandview property.

The REALTOR® was approached by an unrepresented prospective buyer who was interested in purchasing the Carter property. The REALTOR® had the prospective buyer sign a Limited Dual Agency Agreement and then prepared an offer to purchase the Carter property. The offer was delivered to the couple together with the Limited Dual Agency Agreement. The couple signed the Limited Dual Agency Agreement, as well as accepted the offer.

For unrelated reasons, the sale did not complete and the Carter property was eventually purchased by another buyer represented by the brokerage. Upon closing, the couple withheld a portion of the brokerage's commission alleging, among other things, a breach of fiduciary duty by the brokerage and the REALTOR®.

The court found that the REALTOR® had acted as a limited dual agent in preparing the offer to purchase before the concept of limited dual agency had been discussed with the couple and before they had consented to the brokerage and REALTOR® acting as limited dual agents. The court concluded that the REALTOR® should have obtained the informed consent of the seller prior to the preparation of the offer. This breach resulted in the brokerage's claim for commission being reduced by half.

Interestingly, the REALTOR® attempted to claim, at trial, that he did not act as the agent of the prospective buyer in preparing the offer to purchase and that the Limited Dual Agency Agreement was entered into "out of an abundance of caution." The court understandably rejected that argument given the wording of the Limited Dual Agency Agreement in which the brokerage acknowledged that it was the agent for both the seller and the buyer.

In addition to the court's finding as to the timing of obtaining the seller's consent to limited dual agency, this case further illustrates the practical challenges associated with limited dual agency.

In this case, limited dual agency could have been avoided as the buyer was unrepresented when the REALTOR® was first approached. The brokerage and REALTOR® could have declined to provide agency representation to the buyer and continued to act as the sole agent of the seller. Given the submissions of the REALTOR® at trial, it is possible that is what was intended.

However, by entering into the Limited Dual Agency Agreement, the brokerage and the REALTOR® became the agent for the buyer as well as the seller. This fundamentally changed the legal relationship the brokerage and REALTOR® had with both the buyer and the seller.

Licensees must be aware of the difference between, and the implications of, acting as a limited dual agent for an unrepresented buyer and not providing agency representation to that buyer.

| 1. |

|

To subscribe to receive BCREA publications such as this one, or to update your email address or current subscriptions, click here.

“Time is of the Essence” Means “Time is of the Essence” #412

By Edward L. Wilson

Lawson Lundell LLP

Many REALTORS® assist buyers in locating and negotiating the purchase of new condominiums in pre-build situations. The developer’s form of contract is generally used and such contracts often provide for staged deposits, often over long periods, which invariably contain “time is of the essence” clauses.

A buyer entered into a typical developer’s form of contract in August 2004 to purchase a condominium in a complex to be built by the developer.1 The contract provided for a purchase price of $1.26 million and a deposit of 25 per cent, payable in three instalments.

The buyer paid the first instalment of $62,750, but paid $75,000 toward the December (second) instalment of $125,500 one month late. The developer wrote to the buyer in early March 2005 demanding payment of the balance of the December instalment by mid-March, but the buyer failed to pay. A further written demand followed in May, insisting on payment of the balance of the December instalment with interest, plus the third instalment of $125,000, by June 15, 2005.

The buyer made no payment in June and the developer's lawyers sent a letter in late June demanding full payment of the outstanding balance of the deposit by early July. The buyer said he did not receive that letter, but paid $50,500 on July 16.

A further letter was sent by the developer’s lawyers on August 17 acknowledging receipt of the $50,500, stating that a balance of $138,416 remained owing and extending the payment date to August 24. That letter also stated: “This is absolutely the last extension offered to you. If you fail to make the payment by such time, our client has instructed us to terminate the Contract immediately and retain the deposit you have paid on account of damages, without further notice to you.” The buyer said he did not receive that letter, either, and that he was shocked when he learned the developer had purported to terminate the contract on August 30. The buyer said he had understood from discussions with the developer that the July payment of $50,500, with payment of the balance in the fall of 2005, was acceptable. The buyer sued for a declaration that the contract was valid and subsisting.

In reversing the trial decision, the Court of Appeal found the right of the developer to cancel the contract on August 30 was governed by clause 7.7 of the purchase contract, which provided that time was of the essence and that the developer had the option of cancelling or electing to complete the transaction in the event of the buyer’s default.2 Unless all amounts were paid when due, the developer could cancel the contract and do so at any time during the continuance of the default, even if the developer had previously elected to complete the transaction. Clause 7.7 was perhaps harsh from a buyer’s perspective, but it was not commercially unsustainable and the parties had agreed to it. The contract was properly brought to an end.

The message for buyers (and their REALTORS®) is simple: deposits must be paid on time. The dates established for payment of deposits are not mere suggestions, but must be complied with strictly; otherwise, the deposit and the contract are at risk. When advising developers, REALTORS® should carefully administer the receipt of deposits and document any late payments, discussions about extensions or waivers of strict compliance of the terms of the contract and demands for payment.

| 1. | Hinkson Holdings Ltd. v. Silver Sea Developments Limited Partnership, 2007 BCSC 118. | |

| 2. | Hinkson Holdings Ltd. v. Silver Sea Developments Limited Partnership, 2007 BCCA 408. |

To subscribe to receive BCREA publications such as this one, or to update your email address or current subscriptions, click here.

“And/or Nominee” and “And/or Assignee” #65

By Gerry Neely

B.A. LL.B.

A request has been received for an update of the current law relating to the use of the above phrases in the preparation and enforcement of interim agreements.

Column No. 3 written March, 1981, referred to a case where an offer to purchase made by "the undersigned, Century 21 Real Estate Ltd. or nominee" was held to be unenforceable. One reason for this decision was the uncertainty as to who was the intended purchaser. The transaction was quite unusual in that the vendor retained the right to arrange the first and second mortgage financing required to pay out the vendor. This meant that the identification of the purchaser was important since it was his financial strength or creditworthiness that would determine whether the financing would be made available.

Since that case, there have been five reported decisions in British Columbia of which I am aware, in which one party to an agreement to purchase land has argued that these phrases render the agreements void for uncertainty. The uncertainty cases appear to have sprung from a case in which a proposed tenant entered into an agreement to lease with the landlord. The tenant stated that he did not intend to be personally liable, but that the liability would be that of a company to be incorporated by him. The landlord had a different understanding as to the liability of the tenant, and the Court concluded that the uncertainty created by these difference understandings meant that no contract had been concluded and the tenant was absolved from any personal liability.1

A general rule seems to be evolving from the most recent decisions in the cases where the argument was unsuccessful. That rule is that if it can be established that the purchaser's decision to nominate someone else to take title is not intended to relieve the purchaser of his obligations toward the vendor, then the agreement is not void for uncertainty.2

An example would be circumstances in which the purchaser intends to incorporate a company to take title, but understands that he remains liable personally until that happens.If, however, the evidence establishes that the purchaser never intended to bind himself in contract to the vendor personally, but instead intended that the vendor and a third party to be nominated by the purchaser were to contract with each other, then the contract would probably be void for uncertainty. An example of this is the landlord/tenant case referred to above.

The problem in putting this rule into practice is the difficulty in proving the intentions of the purchaser. If a purchaser wishes to have a nominee take title, then to avoid the uncertainty argument, the agreement should contain a sentence similar to the following:

"The purchaser agrees to remain liable to the vendor under this agreement notwithstanding that the purchaser may nominate a third party to complete this purchase."

If the vendor intends to take back a mortgage, then the sentence could be amended as follows:

"The purchaser agrees to remain liable to the vendor not only under this agreement but also as a guarantor under the said (first) (second) mortgage notwithstanding that the purchaser may nominate a third party to complete this purchase."

| 1. | Causeway Shopping Centre Ltd. v. Muise, (1967) 63 D.L.R. (2d) 26, affirmed 70 D.L.R. (2d) 720. | |

| 2. | Kemp v. Lee, 44 B.C.L.R. p. 172. |

To subscribe to receive BCREA publications such as this one, or to update your email address or current subscriptions, click here.

“Best Efforts” Cases #9

By Gerry Neely

B.A. LL.B.

Very occasionally a prospective purchaser for whom an offer to purchase is being prepared, asks for the insertion of a condition in the agreement such as "subject to financing..." because he is not entirely certain whether he wants to buy the property. The reasoning of course is that if he decides that he doesn't want it, the condition precedent prevents the contract from becoming binding, even though financing would be available. This stratagem may not be used as much or at least will be used more carefully, if knowledge of two decisions of the Supreme Court of British Columbia becomes more widespread.

In one, prospective purchasers sought the return of a $50,000.00 deposit paid under a letter of agreement between the parties. The deposit was paid on condition that it would be refunded should the proposed sale fail "due to no fault" of the purchasers. They claimed the sale fell through because they could not obtain financing, and that this was due to no fault on their part. The Court interpreted "fault" as meaning that the purchasers had to use their "best efforts" to meet all of the conditions which would have enabled the sale to be completed. The onus was on the purchasers to show why their efforts to obtain financing had failed. Their own evidence of their attempt to obtain financing through the Federal Business Development Bank satisfied the Court that their failure to obtain financing was due to their failure to present an unusual proposition in a business-like way.1

The second case dealt with a complicated agreement involving a land assembly by a developer for the expansion of an existing shopping centre owned by the developer. There were a number of conditions in the agreement, including obtaining zoning approval, a building permit and final approvals from the municipality and Province for the expansion of the shopping centre by July 31st, 1979. Failing satisfaction of these conditions, the land developer had the option of declaring the agreement null and void. In mid-April 1979, the land developer decided to abandon the idea of the expansion, primarily because of his difficulty in finding an anchor tenant. That had not been one of the conditions to which the agreement was subject. In August, the land developer declared the agreement null and void and the vendor sued for specific performance or in the alternative, for damages.

The vendor was successful, the Court holding that there was an implied obligation on the part of the land developer to use its "best efforts" to bring about the fulfillment of the conditions in the agreement of purchase and sale. By failing to take any bona fide action from mid-April on, to bring about the proposed development, the land developer breached this implied obligation. The agreement was subject to the purchase by the land developer of properties from two owners of lands other than the Vendor who was sued. The Court found that the land developer had not made any concerted effort to purchase those properties. It held that the land developer could not rely on its own failure to use its best efforts to purchase, as an excuse for non-fulfillment of its obligation.2

| 1. | Thorsten and Tate v. Gill,19 B.C.L.R. 389. | |

| 2. | BEM Enterprises Ltd. v. Campeau Corporation, 24 B.C.L.R. 244. |

To subscribe to receive BCREA publications such as this one, or to update your email address or current subscriptions, click here.

“Cooling Off Period” With No Details Creates Uncertainty and Concern in Real Estate Sector

In November, the BC Government announced it will be introducing a “cooling off period” for real estate transactions involving residential resale properties and newly built homes in BC beginning next spring. BC Minister of Finance Selina Robinson announced the policy without any details or advanced consultation with the public or real estate sector, resulting in significant confusion and uncertainty both within the sector and amongst the public. This lack of advance planning has led to concerns that this policy and others under consideration could result in unintended negative consequences for buyers and sellers.

“From the day this measure was announced, real estate brokers and real estate boards in BC have been inundated with questions about how this upcoming measure is going to affect their day-to-day work and their clients,” says British Columbia Real Estate Association (BCREA) Chief Executive Officer Darlene K. Hyde. “While we would have liked to answer these questions clearly and concisely, we simply can’t because of the way this decision was made. There really are no answers yet and that’s causing a lot of concern.”

Recent media reports have erroneously made suggestions that the new “cooling off period,” also known as a recission period, will adopt the same parameters as the seven-day period already in place for pre-construction condominium sales, adding to the uncertainty caused by this announcement.

“The assumptions we are seeing are untrue and are purely a result of the lack of information out there about what could be a substantial change to the real estate transaction,” Hyde adds. “Instead of educating Realtors and the public, we now have to focus on stopping rumours . All this could have been avoided if proper processes were followed prior to this decision being made.”

BCREA supports thoughtfully designed, properly-vettedand evidence-based policy that protects consumers and enhances professionalism and transparency within the real estate sector. Policies addressing market conditions should consider the interests of all parties in a transaction, changing market conditions, regional nuances, potential unintended consequences and should also include a defined process to monitor efficacy of the measures introduced.

Prior to further decisions being made on a “cooling off period” or any other measures related to the real estate transaction or market, it is imperative that thorough consultation with the real estate sector and research is conducted in advance to address factors that may negatively impact home buyers and sellers in BC.

-30-

For more information:

Shaheed Devji

BCREA Senior Communications Specialist

778.847.7424

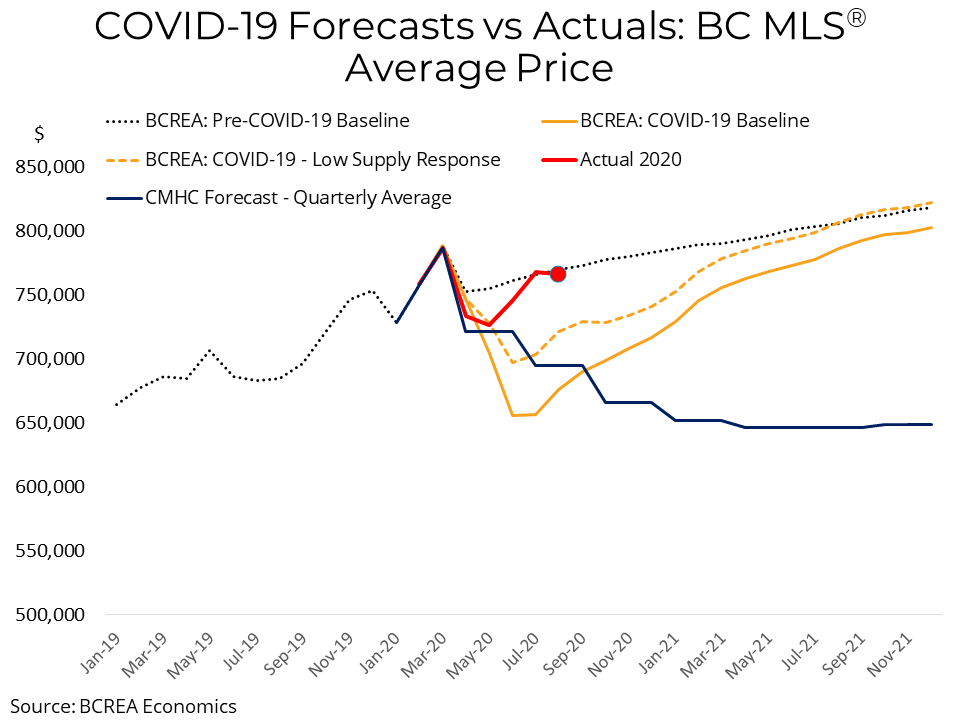

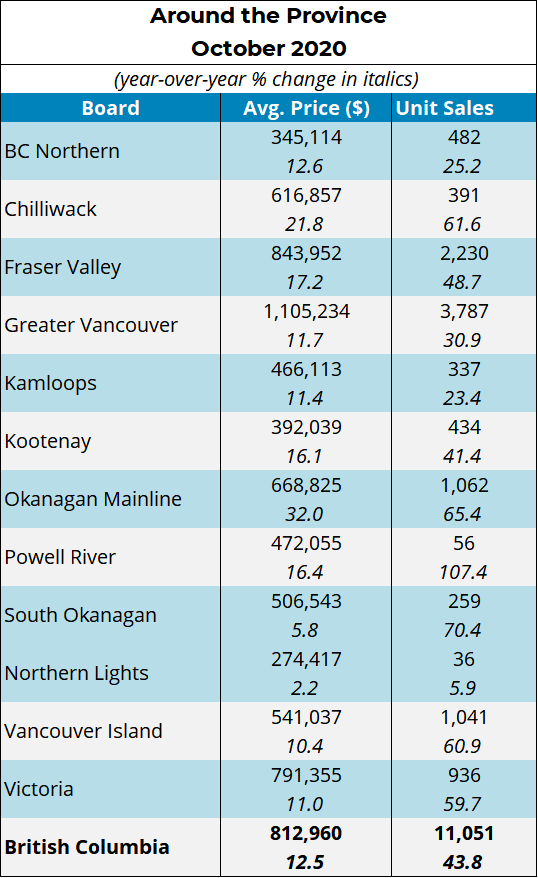

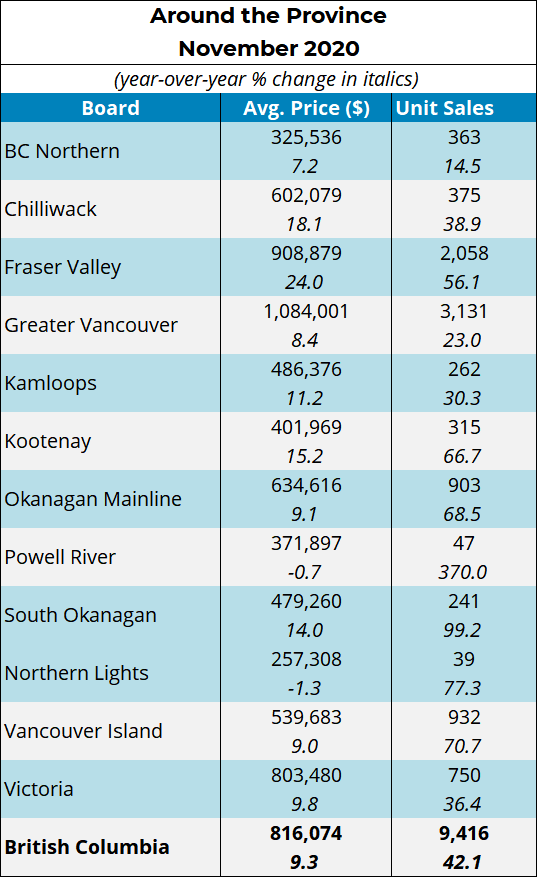

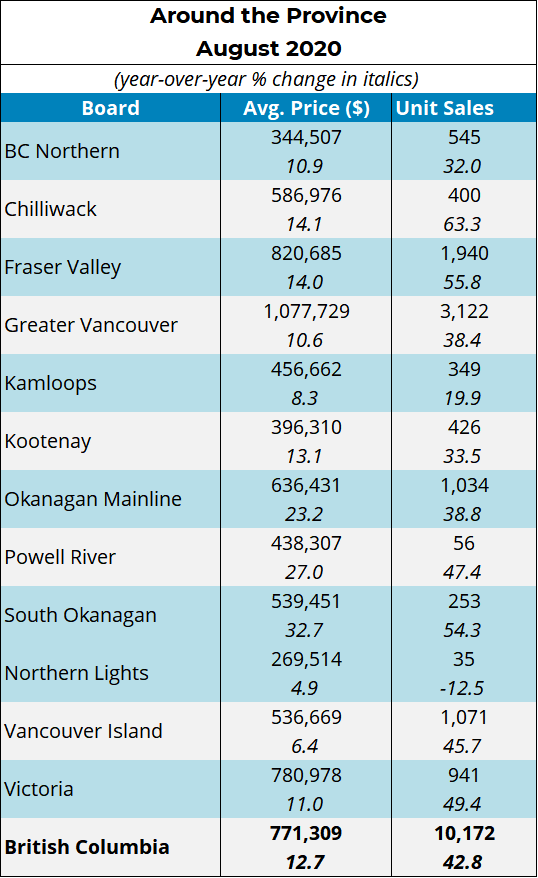

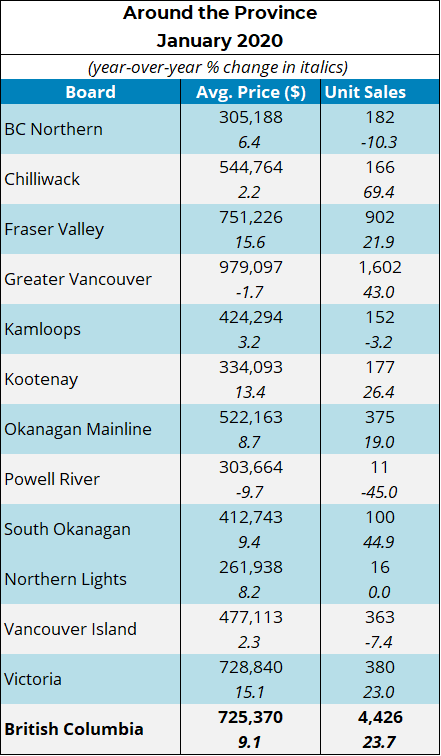

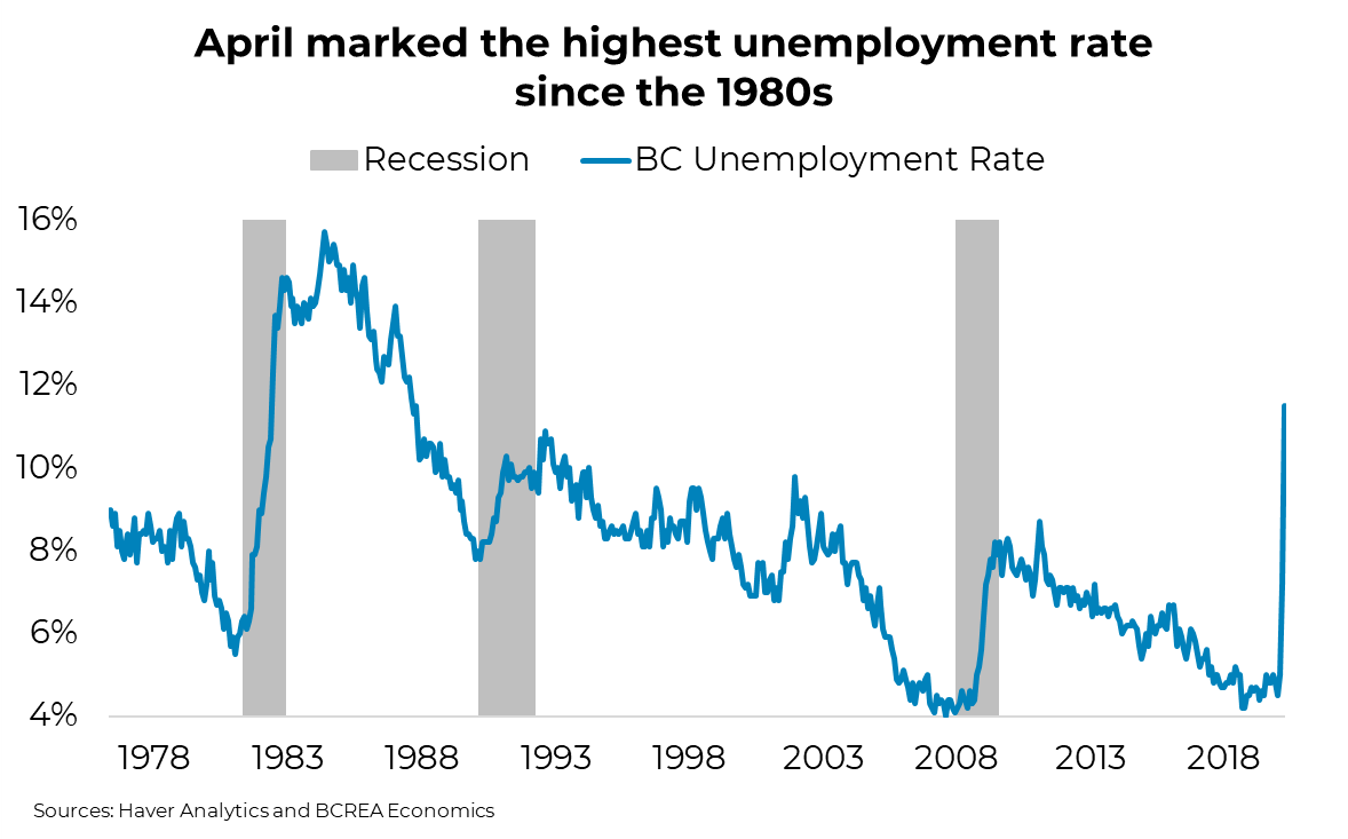

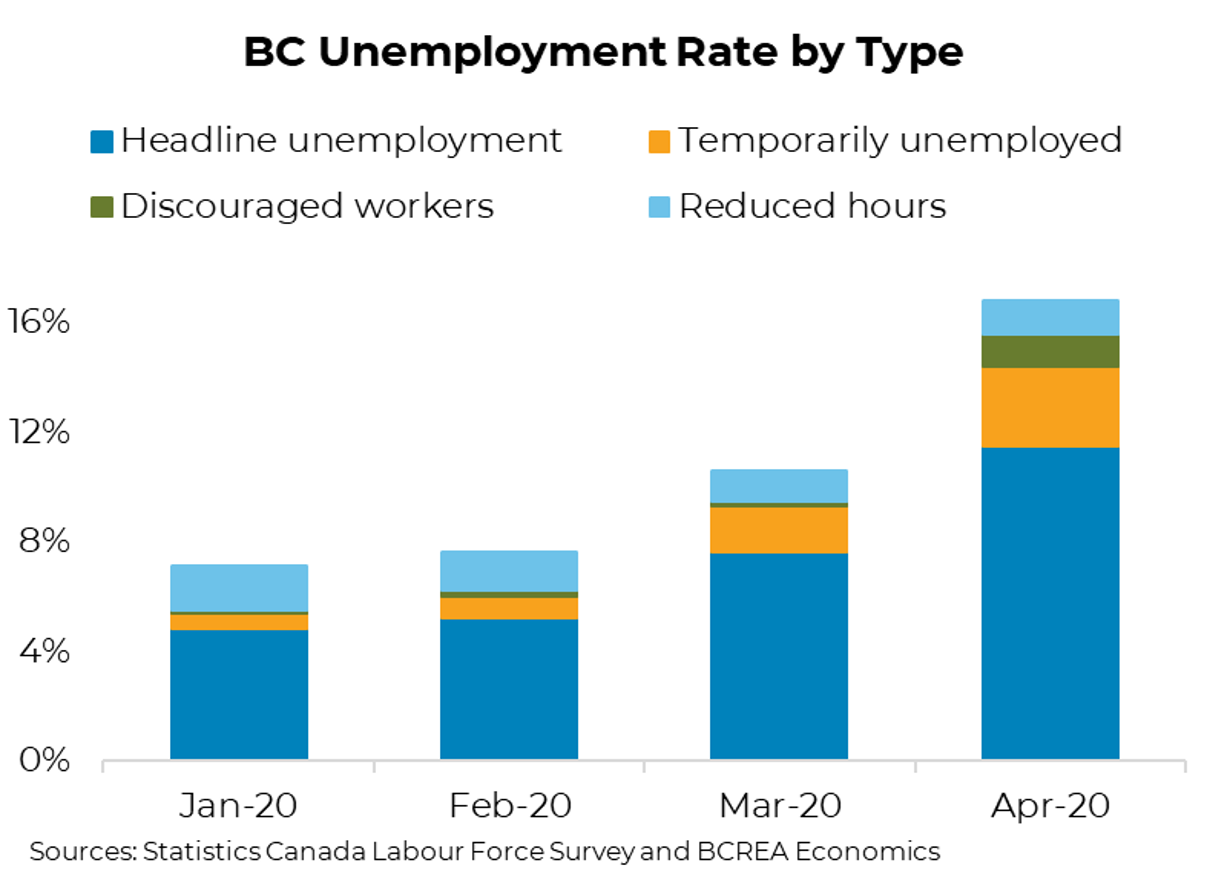

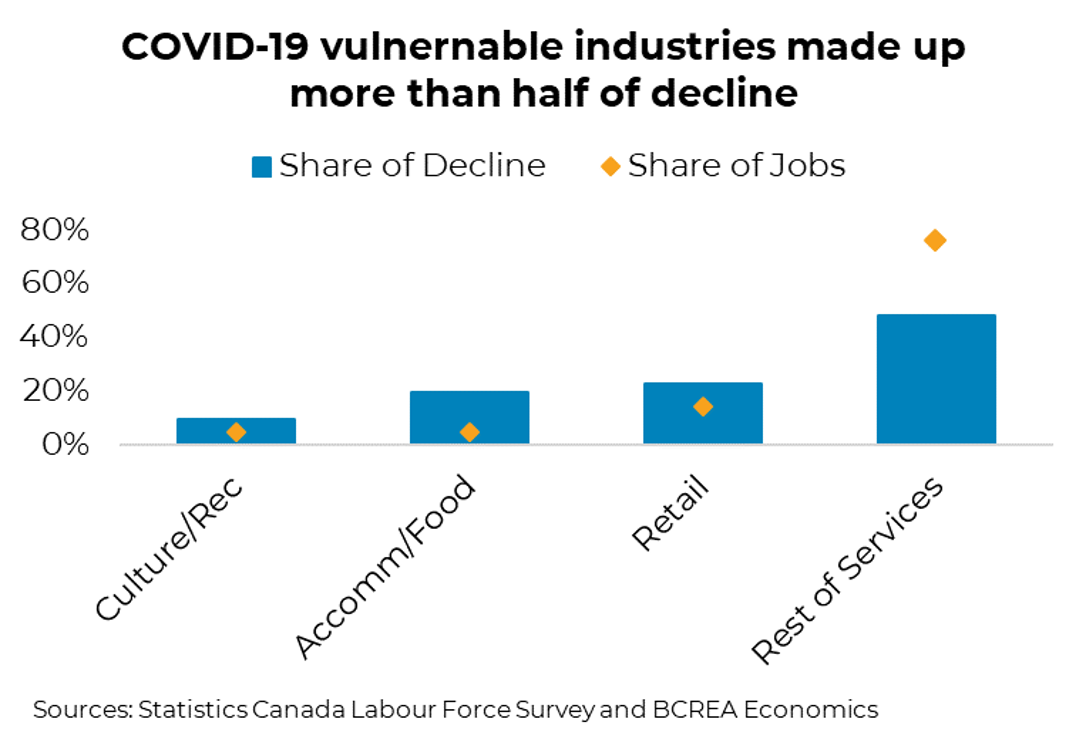

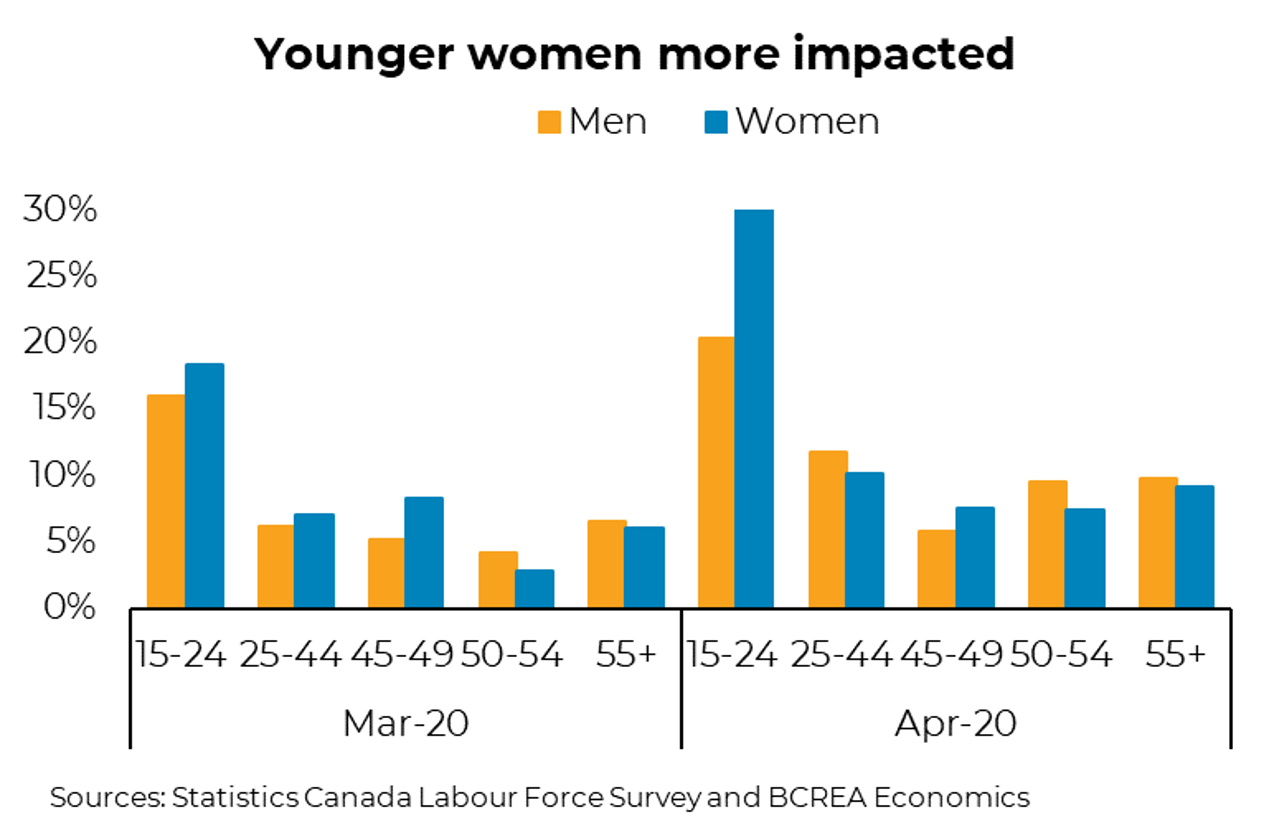

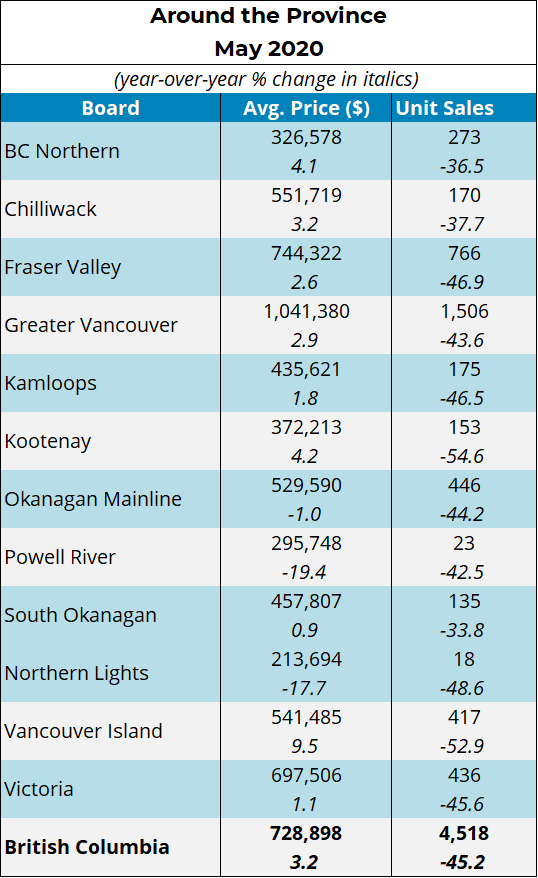

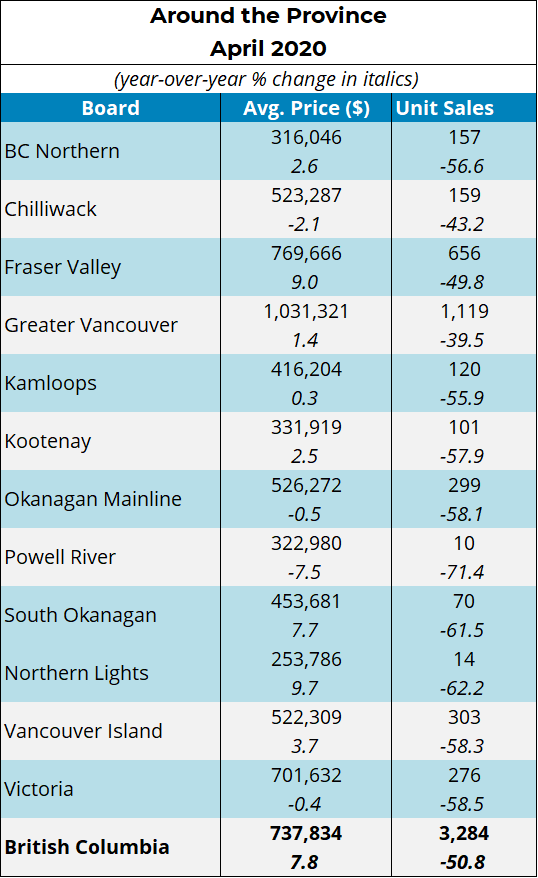

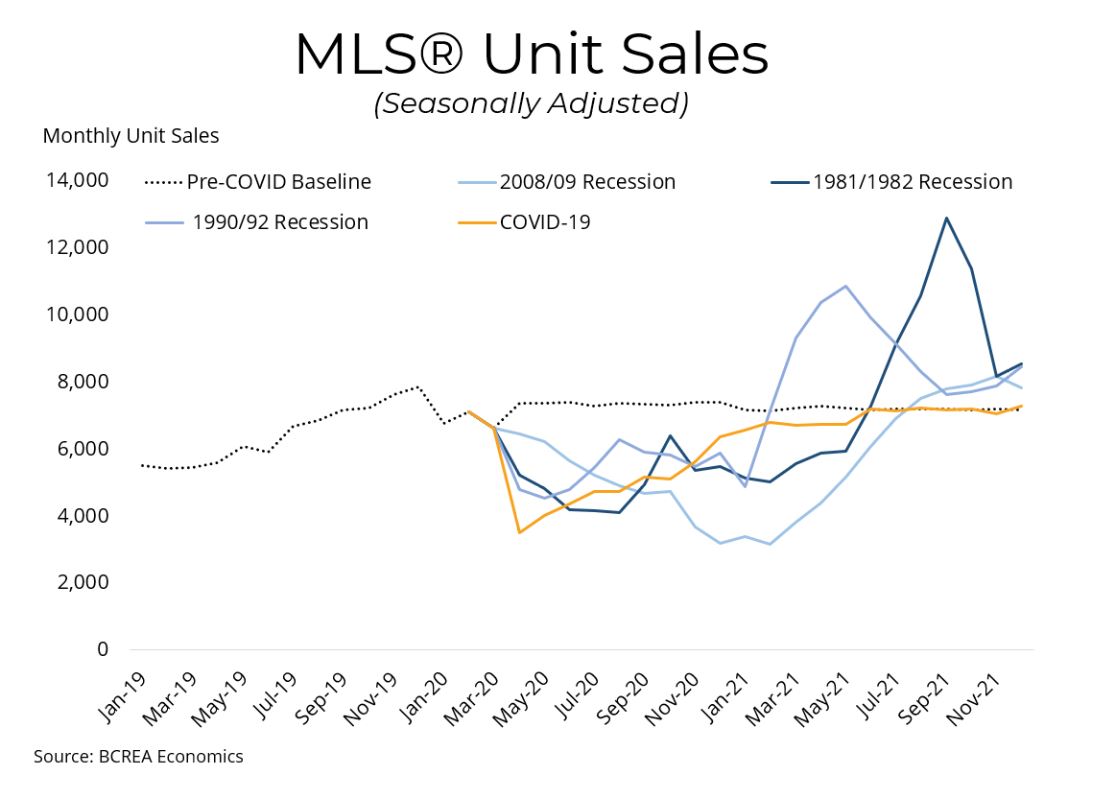

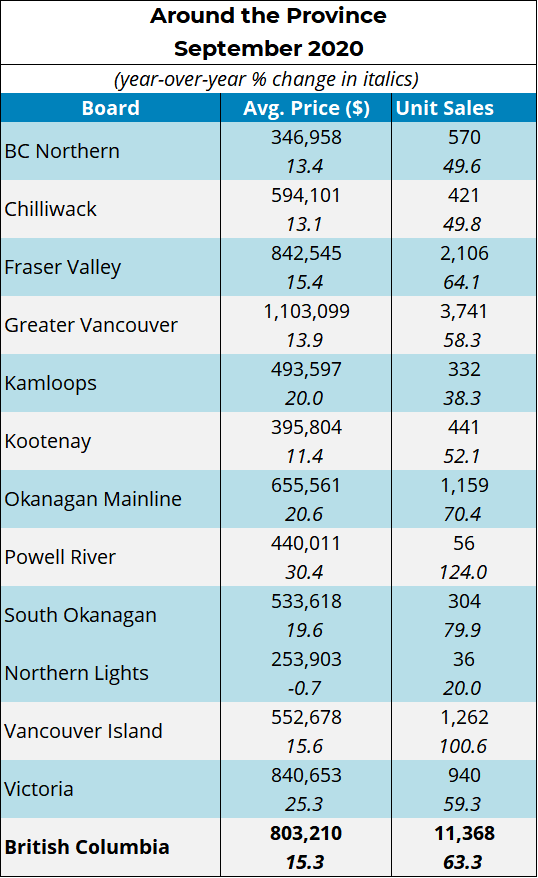

“The Unusual World of Pandemic Economics” – Why BC’s Housing Market Remains Strong Despite COVID-19

Vancouver, BC – September 9, 2020. The British Columbia Real Estate Association’s (BCREA) latest Market Intelligence report, The Unusual World of Pandemic Economics, points to uneven job losses across sectors, an increase in many households’ rate of savings, swift government aid, a tighter-than-ever housing supply and low interest rates as the drivers behind BC’s recent housing market highs.

“The COVID-19 recession has battered many sectors of the BC economy. However, looking at recent data in the housing market, it would be difficult to tell there was a recession at all,” says BCREA Chief Economist Brendon Ogmundson. “In a typical recession, we would see falling demand and rising supply, but this recession is anything but typical.”

Previous BCREA forecasts anticipated housing prices would return to the pre-COVID-19 baseline in early 2021. However, a surge of pent-up demand into an undersupplied market has prices at pre-COVID-19 levels well ahead of schedule.

“Pandemic economics are proving to be very unusual. Many of the trends we are seeing are without precedent and significant uncertainty remains, but we are cautiously optimistic that this housing recovery will continue,” notes Ogmundson.

To read the full report, click here.

-30-

For the PDF of this news release click here.

For media enquiries:

Shaheed Devji

Marketing Communications Specialist

[email protected]

604.757.7260

To subscribe to receive BCREA publications, or to update your email address or current subscriptions, click here.

<em>Heritage Conservation Act</em> Transformation Project Survey

The following letter was emailed to all BC REALTORS® on Friday, September 19, 2025.

Dear BC REALTORS®,

As you may be aware, the provincial government has begun the public phase of engagement on the Heritage Conservation Act Transformation Project (HCATP). The stated aim is to update the Heritage Conservation Act (HCA) to ensure it is consistent with the United Nations Declaration on the Rights of Indigenous Peoples and improve its implementation in a way that benefits all people in BC.

For years, First Nations and stakeholders have raised challenges with the HCA and its administration. Significant changes have not been made to the HCA since 1996. Several concerns have been raised within BC’s real estate sector regarding the province’s current heritage conservation approach as well as the proposed changes that this stage of engagement centres upon.

Reconciliation is an important process that we support, but it’s essential to conduct this work in parallel with the development of much-needed housing in this province. We are concerned with a variety of aspects related to the proposed HCA changes to the degree that we believe the HCATP process should be paused immediately, and a plan put in place to increase consultation and examination of these potential issues.

We would urge you to review and echo these concerns within the framework of the public consultation, which includes an easy-to-access survey (more on that at the bottom of this email).

Broadly, we are adamantly opposed to archaeological data checks being conducted by REALTORS® before property sales because:

- REALTORS® are responsible only for a fraction of all property sales in the province,

- the majority of property sales, including apartment and townhouse stratas, would not benefit from an archaeological data check, and

- the sale of a property does not automatically suggest that an archaeological data check will be of any benefit at all.

Proposed HCA Changes and BCREA’s Top Concerns

We have outlined our additional concerns in point form below:

- Questionable Necessity of the Project: At the outset, we question the necessity of this “transformative” project and suggest the rationale for it has not been adequately established. There are a number of checks and balances already in place to ensure the protection of heritage and cultural assets. While most would agree that these can be strengthened, streamlined, and otherwise improved, we do not see the need for a “transformative” approach.

Specifically, an array of tools and processes already exists to manage heritage considerations within real estate transactions. REALTORS® and consumers can, and in many cases do, already request archaeological information as part of their due diligence; buyers can include conditions in contracts to allow for further investigation; and those with clear development intentions can commission their own archaeological assessments. Local governments also have the authority to require these assessments as part of subdivision or development approvals. We would ask that the specific shortcomings of the existing process be clearly identified, and a thorough, thoughtful discussion take place to address these issues. - Lack of Government Capacity: In response to direct questioning during the consultation sessions, Ministry of Forests staff responded that there are no plans to add additional staff capacity in order to facilitate the anticipated changes to the process. Given the expanded range of factors that will be considered in each application, the need for heightened enforcement, and the expected level of public and sector communication, engagement, and training, delays in permit processing would increase to untenable levels without significant expansion of staff capacity. In the consultation, there were no indications of advance research into a market-practical manner to develop and enact this initiative, which, as structured, seems poised to cause major issues for the housing sector.

- Point of Sale Issues: The above point is particularly significant if archaeological assessments are made mandatory at the time of sale. This would be a problematic policy for several reasons. It places an excessive burden on property sellers, particularly if the transaction represents a distress sale where the property must be sold quickly. As an alternate approach, if an accurate, easily accessible mapping tool or database were available, the data check could be undertaken at a time when it makes the most sense, when a buyer is looking to acquire the property as part of their due diligence, or where a permit for development (a new project, or an expansion / renovation) is being considered. If accurate intelligence is available at any time via a map / database, then the need to provide a check at transaction becomes moot, and there is no threat to the timeliness of a transaction due to any potential delays in completing the data check. We suggest abandoning the “point of sale” completely as it is neither efficient nor does it make use of existing technology.

- Unintended Housing Supply Consequences: The need to create additional housing supply has been a priority of the provincial government for several years, as part of the solution to BC’s affordability issues. Several major pieces of legislation have been enacted to help accelerate the approval and development of new housing projects. Amendments to the HCA could easily have the unintended consequence of causing extended permitting delays and cancelled property transactions. This would undo much of the positive gains from other housing legislation.

- Policy Abuse and Avoidance Risks: The amendments proposed need to be given a “real world” test. In our experience, in situations where a process is seen by end users as overly onerous, complex, costly, or time-consuming, they will seek loopholes or purposely bypass the process, often resulting in challenging situations for future property owners and First Nations. In the case at hand, some vendors may opt to ignore the advice of their REALTOR® and list the property on their own, choosing to sidestep regulations for identification and disclosure of heritage assets.

- Regulatory Review: Any proposed legislative or regulatory requirements anticipated to involve real estate professionals should be reviewed by the BC Financial Services Authority, the regulator of real estate licensees in the province, as well as BCREA and the province’s eight real estate boards and associations.

- Lack of Archaeology Professional Capacity: There are serious concerns about the capacity of the archaeological profession within the province and their ability to meet the requirements anticipated by the proposed legislation. This situation is analogous to one several years ago during the implementation of the BC Energy Step Code, when concerns were raised by sector stakeholders about the number (and geographic distribution) of Certified Energy Advisors in the province, and their capacity to conduct the energy modelling necessary for the rollout of the Step Code. This concern is not only related to the number of archaeologists, but also their geographic distribution. If remote areas of the province require specialists to be flown in, costs will be escalated for those properties.

Without some type of fee regulation, a shortage of experts could also result in increased fees, simply due to demand for their services exceeding the supply. Based on a ten-year average, there are approximately 45,000 annual sales of detached homes and duplexes in the province. In addition, there are commercial and industrial sales, and leases of crown land for resource development. If each of these transactions were to require an archaeological assessment, it is doubtful that the current supply of qualified professionals would be able to accomplish this task on a timely and cost-effective basis. - Engagement and Education Needed: In order to prevent pushback from property vendors, a comprehensive engagement, communication, and education program explaining the impacts of the HCATP will need to be undertaken. The stakeholder session did not mention an investment in such a plan, without which the rollout of changes will be easily misconstrued and misunderstood, and result in inevitable delays and additional costs, which will likely lead to substantial resentment.

- Problematic Intangible Heritage Definition: It is an absolute necessity that a clear and practical definition of “intangible heritage” be developed along with a transparent process to identify and disclose its presence on properties. Property owners and potential purchasers need access to this information when considering development. In today’s market, many housing proposals are already being withdrawn due to high development costs and financial infeasibility. Housing providers rely on accurate financial pro formas to assess project viability. If the financial obligations tied to “intangible heritage” are unknown until after permit applications – or, worse, only discovered once construction is underway – projects face significant risk of collapse, adding further strain to housing supply.

- Practical Application Needed: The overall structure of the HCATP needs to undergo a process in which the proposed changes are viewed from the perspective of a typical development project. With the understanding that the provincial government has identified improving housing affordability as a key policy objective, a balance must be struck between the objectives of HCATP and housing goals to examine how the changes will impact the approval timeline, development costs, and potential viability of housing projects (including non-market housing).

Make Your Voice Heard!

One of the main reasons I’m writing today is to strongly encourage all BC REALTORS® to respond directly to the government’s public consultation to use your voice to help amplify our concerns around this consequential initiative. Feel free to echo BCREA’s concerns as well as any others you may have. Particularly if you have first-hand experience with the HCA’s implementation, your insights are vital.

You can browse this website for more information about the proposed changes and to access the Heritage Conservation Act Survey. The deadline to complete the survey is Friday, November 14, 2025, at 4 pm PT.

BCREA and various member boards and associations are monitoring these policy changes and actively engaging with the government to ensure REALTORS®’ perspectives are heard in this consultation process. We will share relevant updates and any future engagement opportunities with you as they become available.

Should you have questions, concerns, or general feedback about this topic, please don’t hesitate to contact our department at [email protected].

Sincerely,

Trevor Hargreaves

BCREA Senior VP Government Relations, Policy Research, Marketing & Communications

<em>Heritage Conservation Act</em>: Update on Proposed Changes

In 2025, the provincial government announced a series of intended changes to the Heritage Conservation Act (HCA), which the BC Real Estate Association (BCREA) quickly identified as problematic. BCREA promptly submitted a detailed consultation response and engaged directly with the senior executives and policy staff helming the initiative.

Numerous other organizations voiced their own concerns, with many echoing the same issues we had raised. We worked in close collaboration with a variety of housing organizations to amplify and align our advocacy efforts.

As a result of this collective feedback, the government postponed the introduction of its proposed HCA amendments that had originally been anticipated for spring 2026 to allow for additional time to review feedback and chart a revised course.

On Thursday, March 26, 2026, the Ministry of Forests released a technical policy paper outlining updated proposals for change to the HCA. The revised proposals reflect substantive changes informed by stakeholder feedback, and, to the Ministry’s credit, many of BCREA’s prior concerns have been addressed. Most significantly, the paper does not include the prior references to “intangible heritage.” Protections for culturally significant sites will be addressed through existing agreements or designation processes that require thorough documentation, analysis, and consultation before government decisions are made. This addresses one of the primary issues we identified.

We continue to have concerns regarding the potential application of archaeological checks at point of sale. The originally proposed mandatory archaeological checks at the time of sale would be inefficient and overly burdensome, creating a high risk of delays and transaction uncertainty. Instead of this approach, BCREA has recommended an accessible mapping tool or database that supports due diligence at a time when it makes the most sense.

The technical policy paper outlines the intention to move forward with targeted archaeological data checks that would apply only to building permits or property sales involving ground disturbance, not unaffected properties like upper-floor condos. That said, regulations could still require checks at point of sale or land transfer for certain entities and circumstances, with the intention of improving access to heritage data through third-party systems. BCREA intends to meet with the project team shortly to discuss this proposal in further detail, including how remaining point-of-sale risks can be mitigated in practice.

Another potentially problematic issue was the lack of government capacity to effectively deliver changes as originally proposed. The technical policy paper makes the case that the newly proposed project-based permit model would streamline HCA approvals by reducing duplication and enabling conditional and concurrent authorizations. We will be following up to discuss additional practical specifics on this topic.

We previously raised the need for additional engagement and education, which was acknowledged at various points in the updated proposed changes, with a commitment to further engagement on specific items of interest, such as archaeological data checks.

We also have ongoing concerns around unintended housing supply consequences, policy abuse, and avoidance risks, the need for regulatory review, and the lack of archaeology professional capacity that could cause process constraints.

Although engagement on this file is ongoing, the positive news is that the revised proposals are far less onerous for our sector and more practically designed. We will continue to keep you updated on this file as it evolves, but we’re optimistic about the current direction.

BCREA and organized real estate continue to work diligently to ensure the government takes our concerns seriously as it modernizes the HCA. In particular, we are focused on ensuring that any mandatory archaeological data checks at point of sale are as non-cumbersome as possible. We know this is a concern for you and your clients, as it places an undue burden on sellers, especially in distress sales where properties must be sold quickly.

Please stay tuned for further updates in the coming weeks.

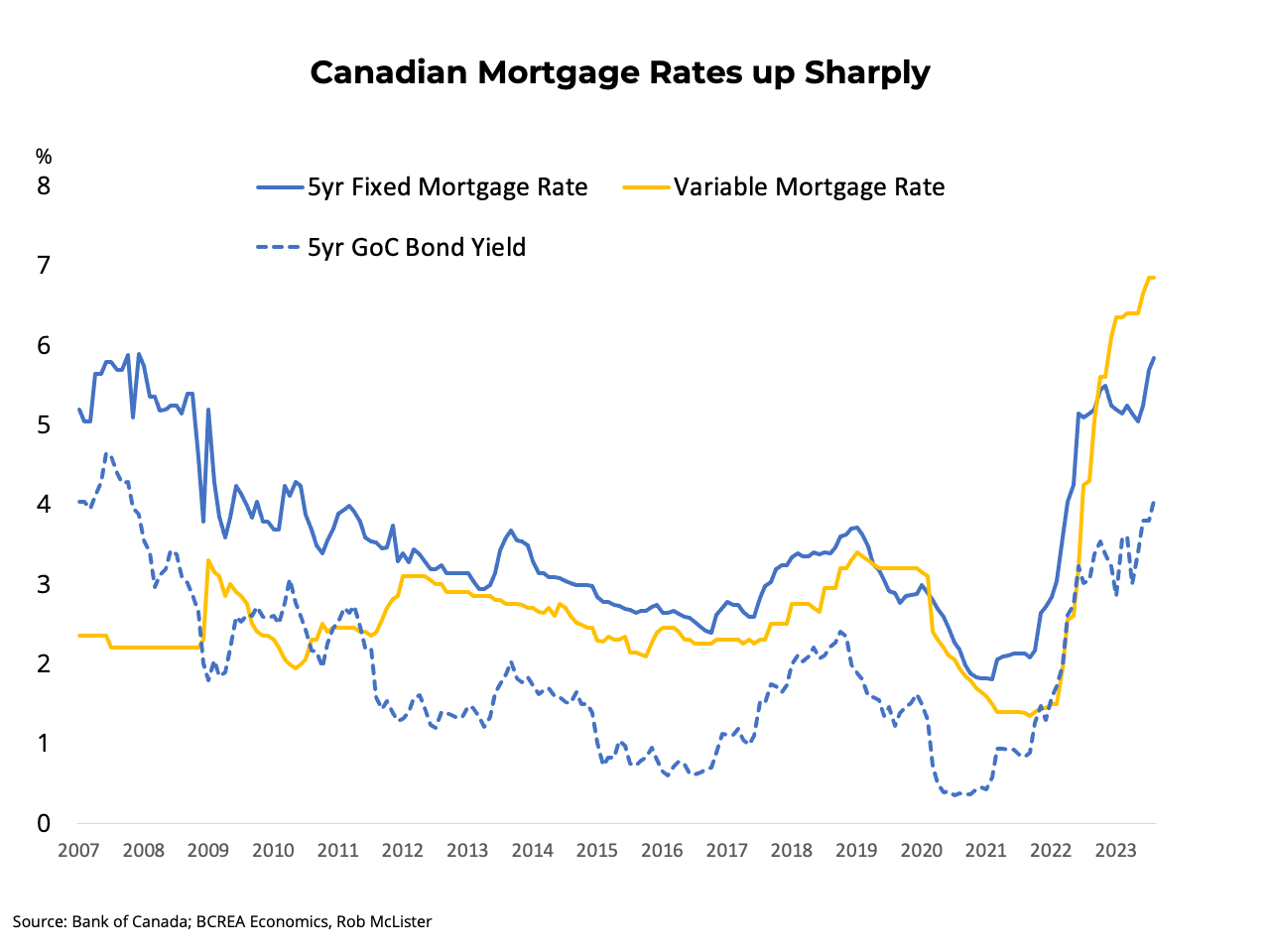

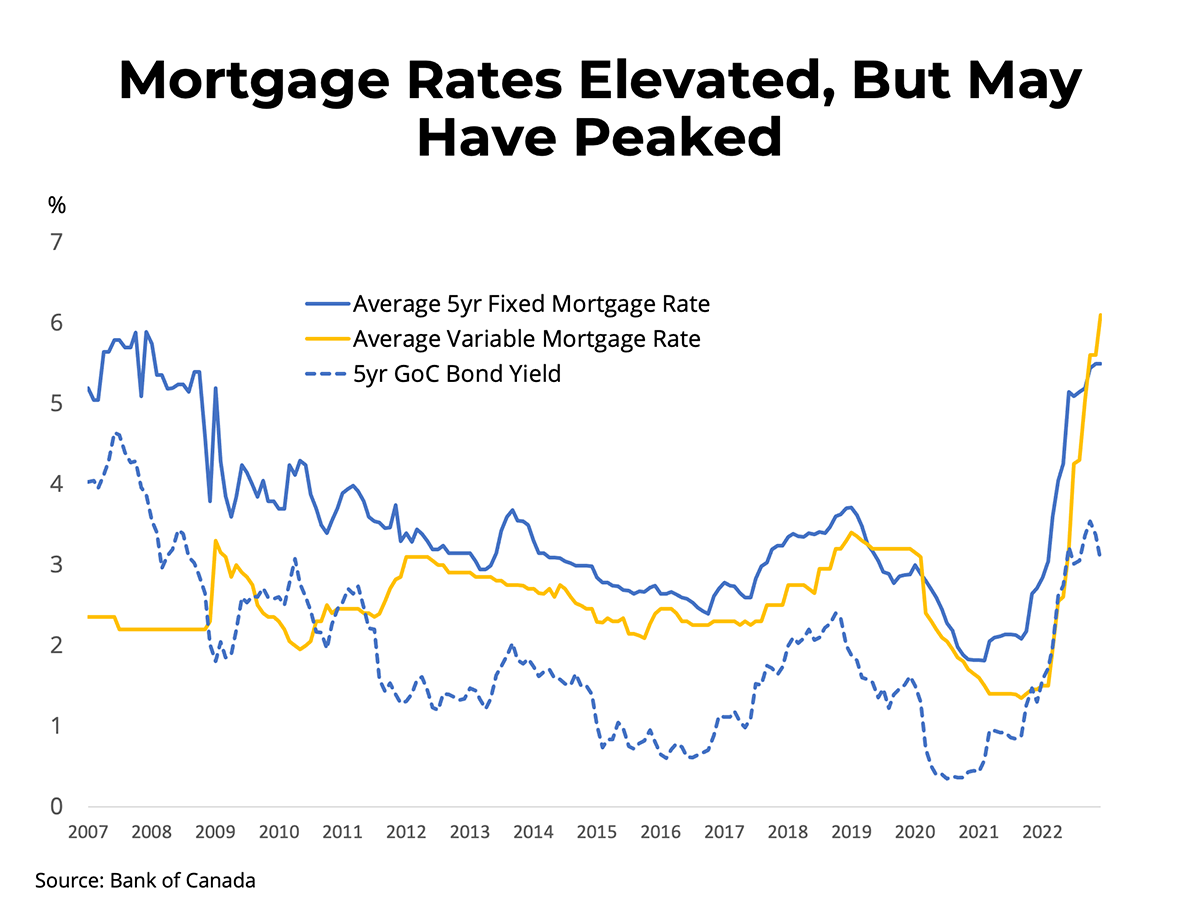

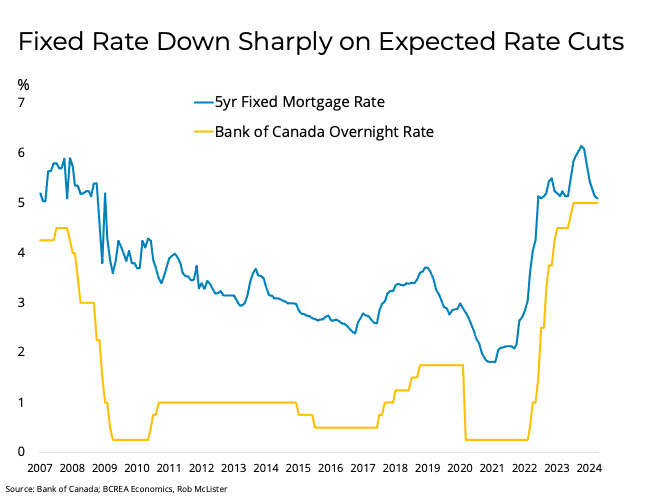

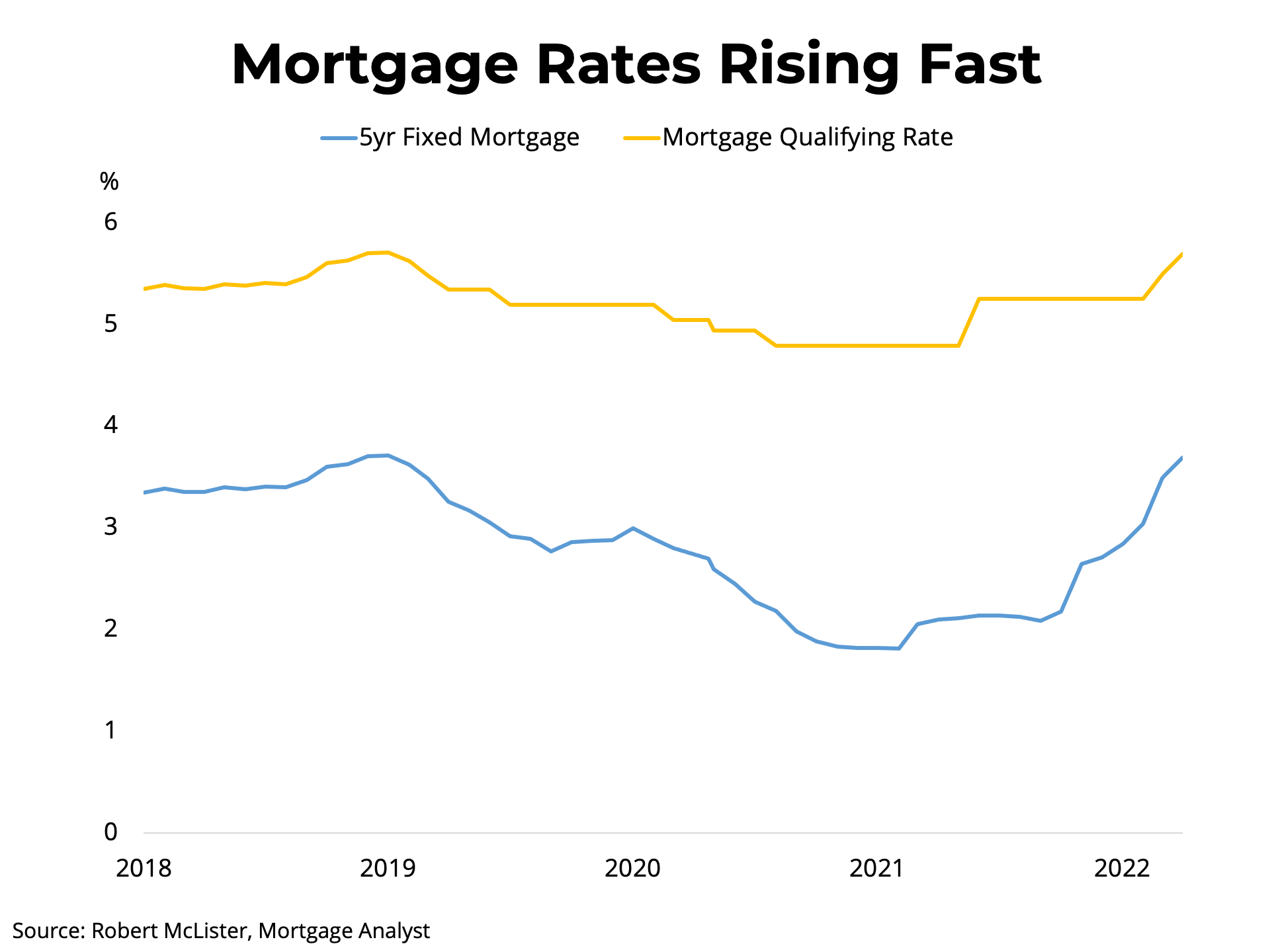

<em>Mortgage Rate Forecast</em>

To download the PDF, click here.

Highlights

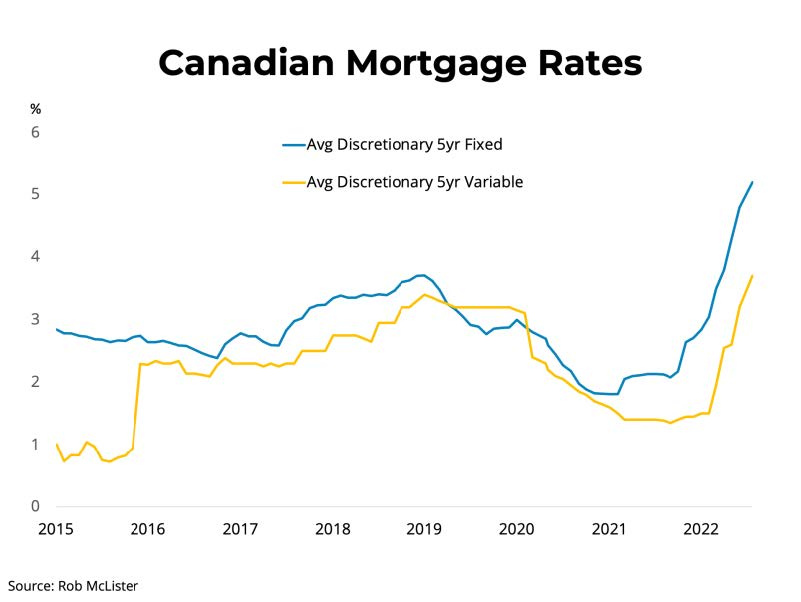

- Canadian fixed mortgage rates are climbing as the oil price shock persists.

- Global conflict and trade uncertainty are pushing growth and inflation in opposite directions.

- The Bank of Canada remains resolute amidst double-sided risks.

Mortgage Rate Outlook

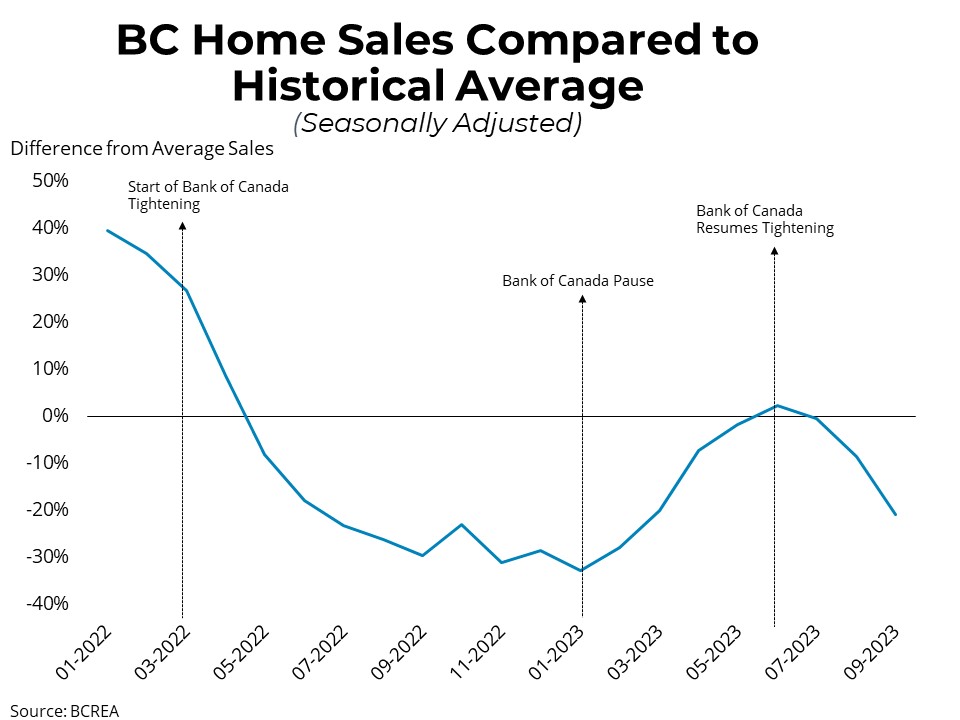

Canadian borrowers were effectively denied a period of lower rates that should have extended through much of 2026. The drop in bond yields seen earlier this year has been erased, as the Iran conflict and ensuing oil shock have driven yields back to early‑2025 levels.

With the Strait of Hormuz remaining under contest, bond markets continue facing upward risks and pressure, pushing fixed mortgage rates to 4.7 per cent. However, a tentative peace agreement between the United States and Iran has unwound some of this pressure. Yields have cooled in recent weeks, underpinned both by the recent peace talks and shifting central bank sentiment, helping to quell inflation concerns.

Given the lack of pass-through so far from spiking energy prices into broader consumer prices, alongside a recovering but still weak Canadian labour market, we may not see a change in the overnight rate this year, despite current expectations of rate increases priced into financial markets. With this in mind, uninsured fixed rates may temporarily retrace to under 4.5 per cent in the short term as yields fall before rising next year as the Bank of Canada returns its overnight rate to 2.75 per cent.

Variable mortgage rates have ticked up after remaining steady across five consecutive rate holds from the Bank of Canada. Lenders have slightly reduced their discounts to protect their margins, pushing rates to 4.2 per cent, roughly 25 basis points below the prime business rate. Overall, the trajectory of variable rates depends on the Bank of Canada’s response to the double-sided risks facing the economy. Given our cautious outlook of the Bank holding throughout the year, we expect variable rates to fall back to 4.1 per cent in 2026 as lenders increase their discounts to levels seen in the spring.

Economic Outlook

The Canadian economy contracted in the first quarter of 2026 by 0.1 per cent on an annualized basis, falling well short of the Bank of Canada’s forecast of 1.5 per cent growth. This contraction was driven by an anomalous surge in non-monetary gold imports and a more concerning drawdown in final domestic demand. Ongoing resilience in household consumption continues to be overpowered by weakening private sector investment.

Recently, tariff and trade uncertainty has been overtaken by the Iran conflict and its oil price shock as the largest concern facing the Canadian economy. The cumulative effect of this shock has raised costs for households and businesses, placing a drag on output. That said, as an oil exporter, Canada may benefit in the short term from higher prices in the global market. Discussions of a resolution may also mitigate some of the impacts from the shock, which would significantly shift the forces driving monetary policy expectations.

Paired with these global challenges is a continued pivot in immigration policy, which has led to a decline in Canada’s population over the past two quarters. Combined with headwinds to domestic demand and trade, the Canadian economy has limited avenues for growth over the forecast horizon. However, the implementation of large-scale federal projects, normalized immigration, and (hopeful) resolutions to trade and the Iran conflicts should steer the Canadian economy onto its traditional growth trajectory in 2028. After contracting for two straight quarters, we expect the economy to rebound modestly over the rest of the year, with about 1 per cent real GDP growth this year and 1.8 per cent in 2027.

Bank of Canada Outlook

Rising inflation stemming from the Iran war has placed the Bank of Canada in an increasingly difficult position. Supply shocks like the closing of the Strait of Hormuz are particularly challenging for central banks because they cannot easily be “looked through” when they are both large in magnitude and persistent. While temporary spikes in commodity prices can often be ignored if policymakers believe inflation expectations will remain anchored and the effects will fade quickly, sustained increases in energy and input costs risk spreading more broadly through the economy via wages, transportation costs, and inflation expectations. In that environment, central banks may feel compelled to tighten monetary policy even as economic growth slows, raising the possibility of a stagflationary economic backdrop.

The Bank of Canada enters this period with considerable institutional credibility earned over decades of successful inflation targeting. Since adopting its inflation-targeting framework in the early 1990s, the Bank has generally maintained confidence that growth in consumer prices would return to target over the medium term. That credibility was tested during the post-pandemic inflation surge, when the Bank was widely perceived to have waited too long to raise interest rates. Critics argued that policymakers underestimated the persistence of inflation pressures tied to supply disruptions, fiscal stimulus, and excess demand. As a result, the Bank may now be more sensitive to upside inflation risks and less willing to delay policy tightening in response to another major global supply shock.

However, with an agreement potentially in place to end the conflict in Iran, pressure to raise rates will certainly ease, and we expect the Bank to look through a temporary supply shock and hold its policy rate at 2.25 per cent this year. That said, because the Bank is at the low end of what it considers neutral for the economy, and because its outlook for growth and inflation assumes a gradual improvement through 2027, there is some upward bias in rates next year. Against this backdrop, the Bank may look to bring its policy rate back to the midpoint of its neutral range, 2.75 per cent.

For more information, please contact:

Brendon Ogmundson

Chief Economist

Direct: 604.742.2796

Mobile: 604.505.6793

[email protected]

Amit Sidhu

Economist

Direct: 604.677.9345

[email protected]

To subscribe to receive BCREA publications such as this one, or to update your email address or current subscriptions, click here.

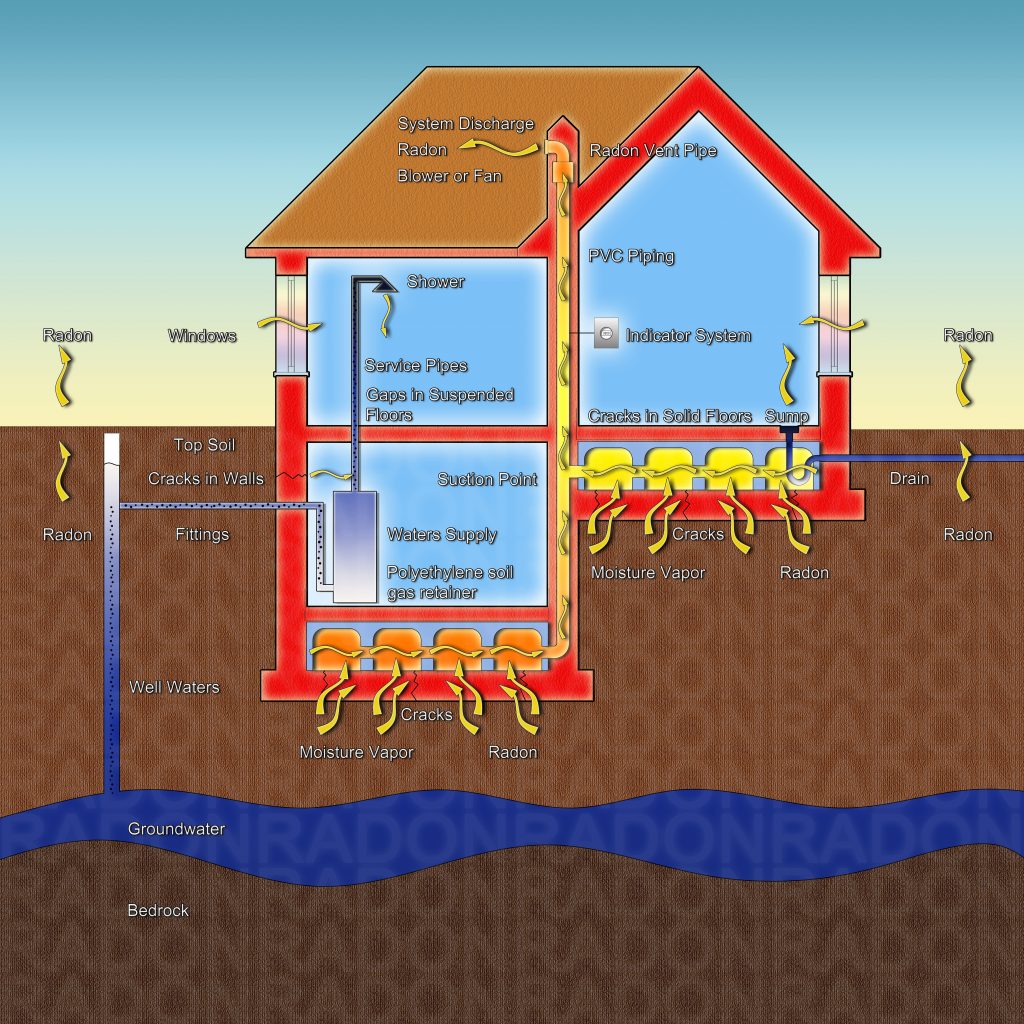

<em>Radon for REALTORS®</em>: Online Course Helps Navigate Radon in Real Estate

BCREA's Radon for REALTORS® online course is worth three accredited PDP hours. In it, REALTORS® explore radon – the leading cause of lung cancer in non-smokers – and how it relates to the real estate transaction.

Radon is a pressing issue, and as a REALTOR® you are expected to demonstrate competency and apply reasonable care and skill when providing real estate services to your clients, which includes being knowledgeable about environmental conditions and taking the appropriate steps to alert clients of known health or environmental concerns.

REALTORS® must recognize that radon measurement is crucial for each home, as radon maps only indicate likelihood, not certainty, and those newer buildings, despite tight construction, may still provide hidden gaps for radon to enter the structure. Testing should span more than 48 hours, considering seasonal fluctuation and the inadequacy of short-term results for accurate assessments.

Learning more about this invisible, odourless gas can help ensure you take the right steps for your clients.

By the end of this course, learners will be able to:

- understand where radon comes from;

- identify how radon enters a dwelling;

- know what influences radon levels;

- locate areas in Canada and in BC with higher exposure to radon;

- recognize the effects of radon on human health;

- understand Canada’s radon awareness initiatives;

- identify applicable laws and emergent policies on radon in BC;

- grasp radon matters in real estate transactions;

- identify the role of REALTORS® around radon;

- understand how a home can be tested for radon; and

- share information on radon mitigation techniques with clients.

Although the primary goal of this course is to provide the radon knowledge REALTORS® need to support and guide clients through a real estate transaction, the information presented can also be valuable for the health and safety of clients and REALTORS® alike.

Learners will earn three accredited PDP hours upon completion of the course. Register here.

"Time is of the Essence" Consideration #215

By Gerry Neely

B.A., LL.B.

One of a licensee's more difficult tasks is setting the date for completion of the sale of property, which is in the process of being subdivided, and to provide for an enforceable extension of closing should registration of the subdivision plan be delayed. Several recent decisions have revolved around the interpretations of clauses giving the vendor or the parties the right to extend the date for closing.

While the developer wants this flexibility, a purchaser, who is prejudiced by delay, will only be able to terminate the contract if the purchaser takes the correct steps in response to multiple extensions of closing not authorized by the contract. What follows may lead you to conclude you have joined Alice and the cheshire cat in Wonderland.

A contract, under discussion in an Ontario case, contained a clause that gave the developer the right to extend the closing date to a date designated by the vendor or the vendor's solicitor.

The vendor extended the closing date, but then followed with seven further extensions over a period of about three months. Three purchasers declined to close, two of whom had raised no objection until they were advised of the eighth extension. All three purchasers argued that since the contract referred "to a date" rather than to "a date or dates", the vendor could only exercise the right to extend the date once.

The judge's agreement with this argument did not help the two purchasers.

The fact that one party is in breach of a fundamental term of a contract does not mean that the contract comes to the end. The other party may elect to keep it in force or to declare it ended. In this case, the two purchasers inaction in the face of the seven extensions was held by the judge to be their election to keep the contract force.

This gave the vendor the right to set the final date for closing contained in the eighth extension. The vendor's notice of this new date when given to the purchasers reinstated "time is of the essence". The two purchasers refusal to close then became their breach of contract which entitled the vendor to damages.

In contrast to the inaction of the two purchasers, the third purchaser objected to the fourth extension. He established a new date for closing which the judge found was reasonable. By doing this the purchaser had established time as being of the essence. This time it was the vendor who rejected the new date for closing, and it was this rejection that enabled the third purchaser to be relieved of any obligations to complete.1

***

In a British Columbia case the clause in the Contract of Purchase and Sale provided for a fixed completion date. If delay was likely, a new date for finalization of the subdivision was to be mutually agreed upon between the vendor and purchaser.

Delay did occur and the vendor requested a twenty-two day extension which the purchaser refused to grant. The vendor then fixed a completion date, approximately six weeks after the date set in the contract, and advised the purchaser of that date. When no response was received the vendor commenced an action for specific performance or damages, put the property back on the market, completed the subdivision and eventually sold the property at a loss.

The purchaser's argument was that the vendor was. unable to complete on the closing date and since the contract stated that time was of the essence, the purchaser was entitled to terminate the contract.

The court rejected the argument, saying that the purchaser's refusal to negotiate with the vendor was a breach of the contract.

The judge's comments with respect to the "time is of the essence" argument was that the extension clause removed the "time is of the essence" requirement. As a result, the vendor acted properly in setting a new and reasonable date upon which the closing would take place and received damages in the amount of $18,500.

In passing the judge also dealt with the inability of the parties to mutually agree upon a new date by saying that it would be open to the court under the circumstances to fix a reasonable time for completion by both parties.2

To subscribe to receive BCREA publications such as this one, or to update your email address or current subscriptions, click here.

Strata Property Act Section 164 – Appeals for Relief Against Significantly Unfair Actions #353

By Gerry Neely

B.A. LL.B

Section 164 of the Strata Property Act gives a strata unit owner or tenant the right to challenge an action completed or threatened, or a decision of a strata council that is "significantly unfair" to the owner or tenant. This phrase has been interpreted to mean that the action complained of ". . . had to be burdensome, harsh, wrongful, lacking in probity or fair dealing, has been done in bad faith, and/or has been unjust and inequitable."1 Several owners tried to use this section over the past year and saw mixed results.

An owner of three strata lots in a recreational development planned to build an exclusive fishing lodge. The plans were frustrated by the passage of a strata bylaw that limited the use of all strata lots to residential purposes. After an analysis of the many uses permitted by the pertinent zoning bylaws and the building scheme, both of which were referred to in the Disclosure Statement, the judge decided that the strata bylaw was significantly unfair and could not be enforced against the owner.2

In another case, the owner of a residential strata unit in a strata corporation that limited rentals applied for relief of hardship under sections 144 and 164 of the Strata Property Act. He had been transferred to Europe and was not prepared to sell his unit at a substantial loss. The limited financial information provided by the owner indicated that his employer paid his basic rent in Europe and that he incurred personal expenses of $1,426 per month. The judge concluded the strata council had acted correctly when it decided the owner failed to show that the rental bylaw caused him hardship.3

The following factors have been relevant for consideration by strata councils in decisions involving hardship claims:

- sale value exceeded purchase price;

- units were purchased for investment and tax shelter purposes, which would have been impeded if units could not be rented;

- inability to sell at various prices and the devaluation of the Canadian dollar vis-à-vis the US dollar;

- economic hardship in conjunction with a "leaky condo" issue;

- units listed for 20 per cent less than purchase price; the financing for these units required the owners to put mortgages on their homes as collateral security, and the owners faced financial ruin if the rental income to service the debt ceased;

- substantial decrease in sale value when a ban on rentals was put in place and the value of the unit is a substantial part of the owner's assets; and

- duplication of monthly expenses arising from the maintenance of two homes; applies to all non-resident owners, but only becomes a consideration for a specific owner if the duplication creates hardship that cannot be avoided or afforded.

To subscribe to receive BCREA publications such as this one, or to update your email address or current subscriptions, click here.

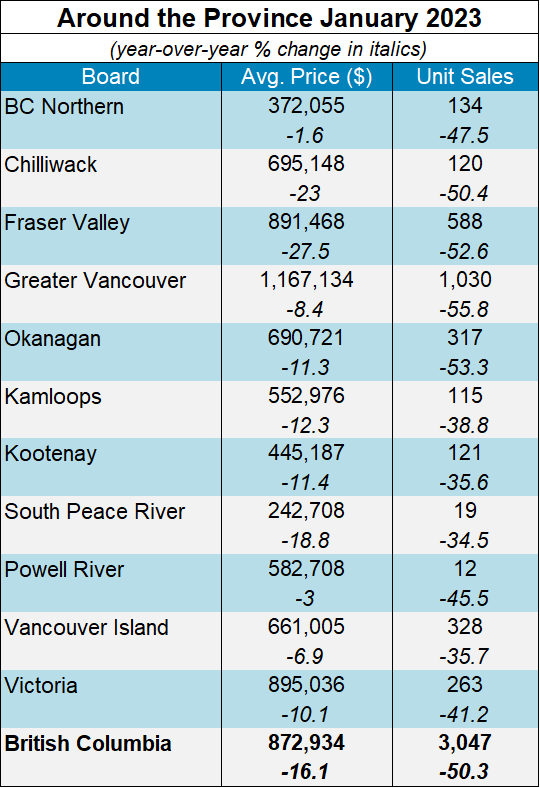

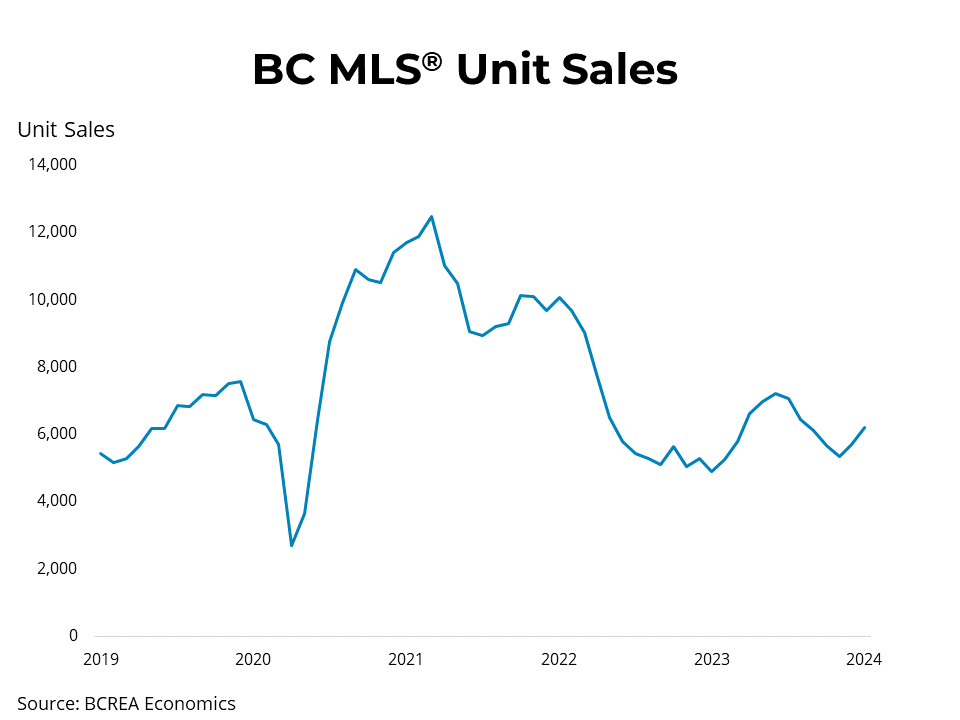

Housing Market Activity Off to a Slow Start in 2023

For the complete news release, including detailed statistics, click here.

Vancouver, BC – February 14, 2023. The British Columbia Real Estate Association (BCREA) reports that a total of 3,047 residential unit sales were recorded in Multiple Listing Service® (MLS®) systems in January 2023, a decrease of 50.3 per cent from January 2022. The average MLS® residential price in BC in 2023 has seen a dip to $872,934, down 16.1% compared to the average price of over $1 million in January 2022, which was recorded near the peak of the market. The total sales dollar volume was $2.7 billion, representing a 58.3% decrease from the same time in the previous year.

“Provincial sales are off to a slow start in 2023 as activity continues to be weighed down by high borrowing costs,” said BCREA Chief Economist Brendon Ogmundson. “While average prices have flattened out in many markets over the past few months, year-over-year measures reflect the decline that occurred from the peak in 2022, as well as a marked shift in the composition of sales away from more expensive homes.”

The total number of active listings has significantly increased compared to the record low level recorded at the start of 2022. However, at just under 22,000 total listings, the inventory of homes for sales remains well below normal for January as a scarcity of new listings in many markets has muted the impact of slow sales activity.

-30-

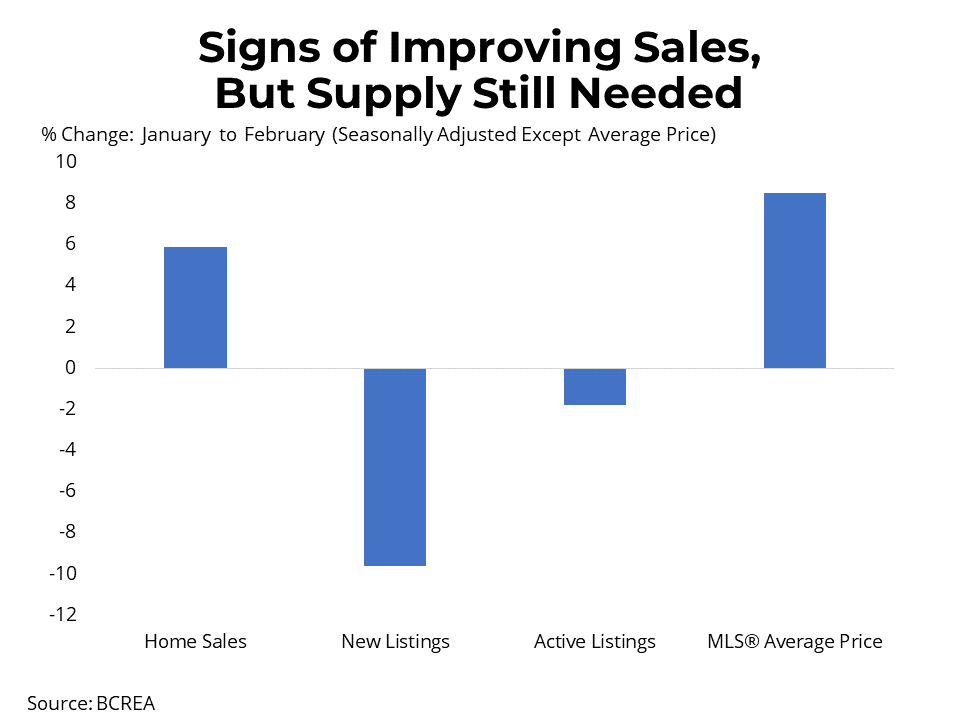

Provincial Housing Market Showing Signs of Recovery Heading into Spring

For the complete news release, including detailed statistics, click here.

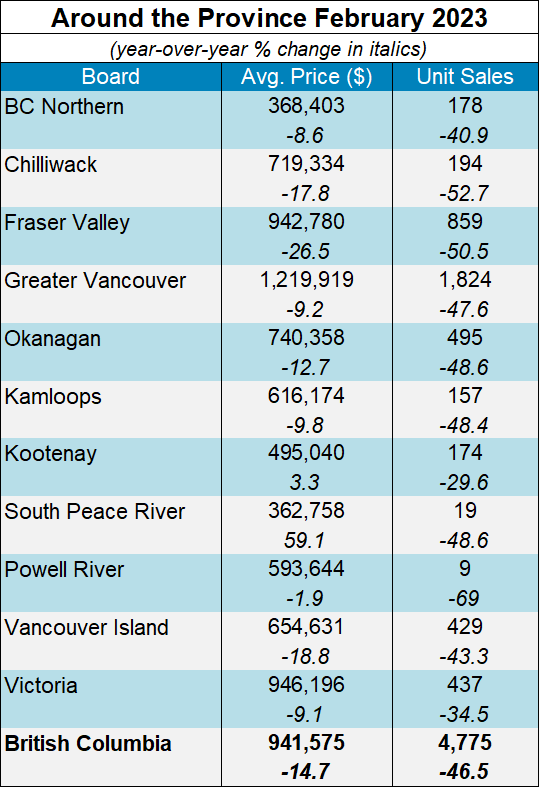

Vancouver, BC – March 13, 2023. The British Columbia Real Estate Association (BCREA) reports that a total of 4,775 residential unit sales were recorded in Multiple Listing Service® (MLS®) systems in February 2023, a decrease of 46.5 per cent from February 2022. The average MLS® residential price in BC in 2023 was 941,575, down 14.7 per cent compared to the average price of over $1.1 million in February 2022, recorded at the market's peak. The total sales dollar volume was $4.5 billion, representing a 54.4 per cent decrease from the same time in the previous year.

“While activity across provincial housing markets remains well below normal,” said BCREA Chief Economist Brendon Ogmundson. “There are encouraging signs that the market is balancing out. Home sales rose month-over-month in most markets, and prices appear to be firming up in the face of low supply.”

Worth mentioning, the provincial MLS® average price was up 8.5 per cent month-over-month to its highest level since July 2022, partially due to a more stable market but also because of the composition of sales reverting to a more normal mix following low sales of single detached homes through the Lower Mainland in January.

-30-

2019 BCREA Annual Report Now Available

The 2019 British Columbia Real Estate Association (BCREA) Annual Report is now available for viewing.

This year, the report was created in the form of a microsite and can be accessed at bcreaannualreport.ca.

With 2020 in full swing, the 2019 Annual Report explores the key focus areas and outcomes achieved at BCREA last year in collaboration with our partners. Most importantly, it highlights BCREA's commitment to resiliency, collaboration, and innovation so we can provide the best service to the province's 11 real estate boards and 23,000 REALTORS®.

The report includes:

- a video message from BCREA CEO Darlene Hyde and President Michael Trites,

- a year-in-review video highlighting the key organizational and departmental successes from 2019,

- a feature article with commentary from BCREA staff, and

- a link to the 2019 Audited Financial Statements.

To subscribe to receive BCREA publications, or to update your email address or current subscriptions, click here.

2021 Advocacy Year-In-Review

This year was full of significant changes for the real estate sector in BC. REALTORS® continued to navigate the challenges of the COVID-19 pandemic and many assisted communities hit by historic rainfalls in a number of ways, including fundraising to support the Red Cross.

2021 was also filled with significant government interventions impacting the sector. Here’s a recap of significant actions by the BC Government from this past year.

Cullen Continues Inquiry into Money Laundering

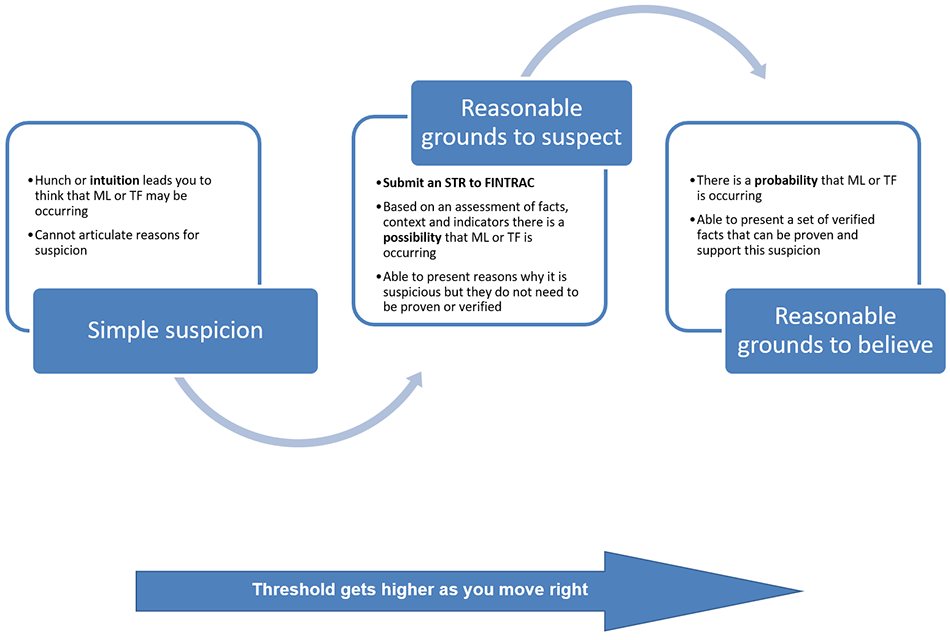

The Commission of Inquiry into Money Laundering in BC (Cullen Commission) continued to examine a series of sectors, including real estate, throughout 2021. BCREA Chief Executive Officer Darlene Hyde and Chief Economist Brendon Ogmundson were participants in the Cullen Commission, during which they answered questions about the real estate sector and demonstrated how BCREA has supported Realtors by equipping them with tools to help identify and combat money laundering. These tools included developing a course for managing brokers and compliance officers, and providing resources on filing Suspicious Transaction Reports and other FINTRAC requirements.

Oral submissions to the Cullen Commission ended in October 2021. The Cullen Commission was recently granted an extension for submitting their final report, which will now be published on May 20, 2022. We look forward to the release of the final report and will continue advocating for smart policy to ensure integrity and transparency in supporting Realtors to help identify and combat money laundering in real estate.

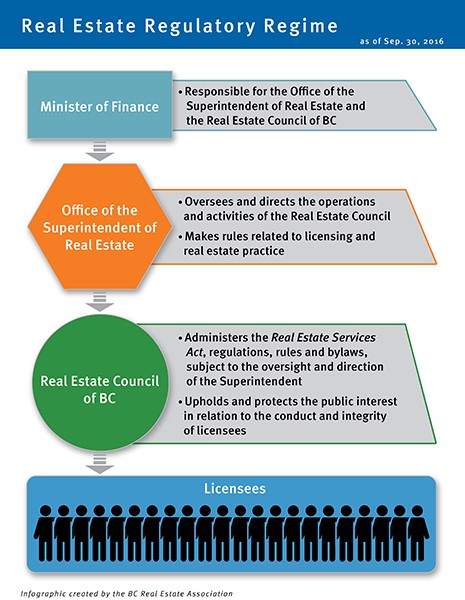

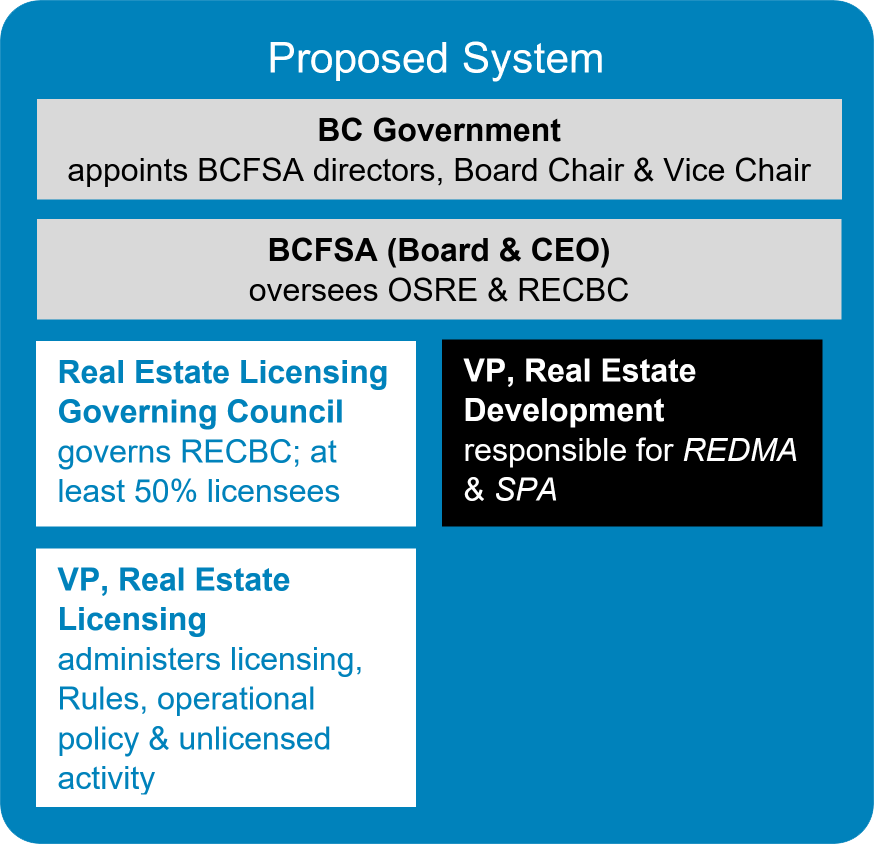

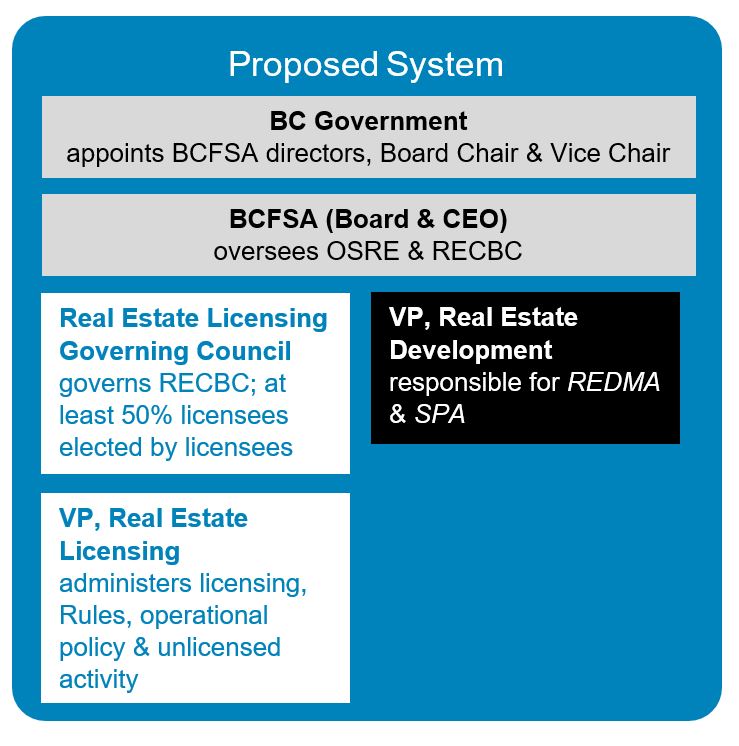

BC Real Estate Sector Moves to Single Regulator

For the second time in five years, the real estate regulatory system was restructured. In March 2021, the government passed amendments to the Real Estate Services Act, resulting in a new regulatory body for real estate, the BC Financial Services Authority (BCFSA). In addition to real estate, BCFSA also regulates credit unions, trust companies, insurance companies, mortgage brokers and pension plans.

At BCREA, we are hopeful about the potential of the shift away from a dual-regulator model, which had its challenges. We do, however, have several ongoing areas of concern that we are continuing to advocate for as we continue regular meetings with senior staff at BCFSA. We will continue to call for the creation of a Professional Standing Committee to establish licensing qualifications and provide on-the-ground insights into all proposed changes to real estate practice.

Actions Taken to Improve Housing Supply

While there is no single solution to housing affordability in BC, governments can have the greatest impact by encouraging increased housing supply. A recent BCREA Market Intelligence report estimates in March 2021, 67,000 buyers were searching for homes across BC while only 24,000 listings were available. In November 2021, total active residential listings were down 40 per cent year-over-year an all-time record low for the province. These numbers highlight the undersupplied housing market in the face of surging demand.

There has, however, been some progress made by the provincial government on increasing housing supply in the past year, including:

- speeding up local government’s development approvals processes by removing the default requirement for local governments to hold public hearings for zoning bylaw amendments that are consistent with Official Community Plans,

- enabling local governments to delegate decisions on minor development variance permits to staff so they can also work towards decreasing approval times and

- providing grants to local governments to create more efficient development approvals processes.

Undoubtedly, there is still much more to be done to reduce the imbalance between housing supply and demand in BC. We are calling for the government to implement other supply-side measures and calls to action made by the Development Approvals Process Review and the Expert Panel on Housing Supply and Affordability alongside fulsome consultation with the real estate sector.

These are just a few significant developments from the BC Government and on which BCREA will continue to focus on closely into the new year. Other policies that will reverberate into 2022 is the recently announced cooling off period and the fallout from the federal election, which included a promise by the Liberal Party to introduce a Home Buyers’ Bill of Rights.

2022 Advocacy Year-in-Review

With 2022 now in the rear-view mirror, BCREA’s Government Relations department reflects on a busy and eventful year.

2022 was filled with regulatory change and shifts in the provincial political landscape impacting the real estate sector. Public and media interest around housing affordability intensified greatly across the year, often portrayed as escalating crises. As a result, governments have felt pressured to act quickly – at times rashly, announcing policies with varying degrees of advanced research and sector collaboration.

Amidst this backdrop, the BCREA Government Relations department has adopted an increasingly research-oriented approach, adding original data and policy research to media and governmental discourse. Our goal has been and continues into 2023 to go beyond asserting opinion, but rather providing evidence-based sectoral thought leadership. Here’s a recap of our activities from the past year.

A Better Way Home

In response to the provincial government’s announcement of a Home Buyer Rescission Period, BCREA released a research-focused white paper titled “A Better Way Home.”

After months of rigorous research and analysis, the report provided 33 recommendations to improve consumer protection and transparency in the real estate transaction process. The report was released in 2022, along with a press conference and a comprehensive communications, public and media engagement plan. The campaign was well-received and extensively covered by national and regional media outlets. Many of the proposals were echoed in the BC Financial Services Authority’s (BCFSA) report “Enhancing Consumer Protection in BC’s Real Estate Market.”

Despite the aligned recommendations of BCREA and the BCFSA, the provincial government moved forward with legislative change announcing that the Home Buyer Rescission Period would take effect in January 2023. Throughout this process, BCREA worked closely with the regulator and other stakeholders to ensure that REALTORS® have the resources to understand and comply with the changes. We continue to monitor this process closely and maintain an ongoing dialogue with the regulator around real and potential issues tied to this legislation.

Provincial Government Leadership

In June 2022, Premier John Horgan announced that he would be stepping down as soon as the BC NDP elected a new leader. After the disqualification of an “outsider” leadership candidate, David Eby was sworn in as premier on November 18. During his campaign, Eby focused much attention on BC’s housing crisis, and echoed many of BCREA’s concerns about a chronic housing undersupply and protracted approval process for new housing projects.

Upon taking office, Premier Eby announced the creation of a stand-alone Ministry of Housing and appointed Ravi Kahlon as its first Minister. Other new and major cabinet portfolios went to Minister of Finance Katrine Conroy, Attorney General Niki Sharma and Minister of Municipal Affairs Anne Kang. Ministers remaining in their portfolios include Minister of Health and Minister Responsible for Francophone Affairs Adrian Dix, Minister of Public Safety and Solicitor General Mike Farnworth, and Minister of Transportation and Public Infrastructure Rob Fleming.

Having worked with Eby closely in recent years, we are optimistic about his approach in the coming year. As a policy forward, hands-on leader, we expect a closer relationship with the Premier’s office and better collaboration around potential policies in the months ahead. This is a much-needed change from the prior administration.

On the issue of housing affordability, we have spent the last few years countering the narrative that BC affordability issues are closely related to foreign ownership. The metrics simply do not support this assertion, given that foreign ownership has fallen to less than 0.5 per cent in the last two years. Our focus has been on demonstrating that a supply drought is the main causal indicator – and we have had strong success in convincing the Minister of Housing (now Premier) David Eby to adopt this position.

Under this lens, our focus increasingly turned to influencing change at the municipal level. A primary challenge point of increasing supply is inefficiencies at the municipal level. To this end, we have been and will continue into 2023 focusing efforts on change at this level of government. Streamlining approval processes, better structures to deal with the “NIMBY” attitude at the community level, and more aligned provincial leadership leveraging provincial and federal funding as being tied to regional development have been particular areas of focus.

Local Government Shake-up

In October 2022, British Columbians went to the polls to elect their local government representatives. A new wave of mayors and councillors brought significant change to many municipalities in the province.

In Victoria, the retirement of Lisa Helps brought wholesale change to council, as Marianne Alto captured the mayoralty, and a virtually entirely new council will helm the city for the next four years.

In Vancouver, Ken Sim rolled over incumbent mayor Kennedy Stewart with a resounding landslide victory, and four new councillors will join the six who were re-elected.

Wholesale change was also the theme in Surrey, with incumbent Doug McCallum and his running mates all but erased from council.

New mayors also won elections in Kelowna, Kamloops, Port Moody, Langley Township, Prince George, and Abbotsford (among others).

Union of BC Municipalities

In September 2022, BCREA attended the annual convention of the Union of BC Municipalities in Whistler. This year, for the first time, BCREA invited its member boards to participate. Real Estate Board of Greater Vancouver has been a long-time attendee on its own, and delegates from Fraser Valley, Interior, Northern and Vancouver Island all participated, making for a strong presence at the convention. BCREA created materials to hand out to delegates and hosted several important meetings on-site with various mayors and provincial officials.

Federal Foreign Buyers Ban

In much the same manner as the provincial Home Buyer Rescission Period, the federal government quickly announced and passed the Foreign Buyers Ban legislation with insufficient research or consultation.

Ottawa’s decision to release the accompanying regulations a mere ten days prior to implementation left REALTORS® across Canada scrambling to understand and comply with the new regulations. Many sectoral thought leaders (including BCREA) have drawn attention to the “political, rather than practical” nature of this policy, which is not expected to have any meaningful impact on its intended purpose to make housing more affordable for average Canadians.

What’s Coming in 2023

BCREA’s Government Relations department anticipates another intensive year amidst governmental pressure tied to issues of national housing affordability. Both the federal and provincial governments are paying particular attention to housing policy issues and are often skirting the necessary research and analysis to draft comprehensive legislation that will achieve stated goals. We will be continuing and expanding detailed, research-based advocacy on behalf of all BC REALTORS®.

We are committed to representing the voice of BC REALTORS® in advocating for the common goals of improving housing, implementing a regulatory system that works for REALTORS® and their clients, and ensuring that policies are based on evidence and adequate consultation.

To get in touch with us, please contact us at [email protected].

2023 Standard Forms Launch

The Standard Forms Launch aims to address the needs of REALTORS® in this dynamic environment by revising and creating new forms and clauses to help support the profession while minimizing the number of changes throughout the year.

Today’s release encompasses updates that ensure BCREA Standard Forms are consistent and reflect current practice requirements and the various requests received from real estate practitioners.

Some highlights of the release include:

- The addition of a new counterparts term,

- New heritage and archaeological questions in the Property Disclosure Statements,

- A new Releasing Trust Account Deposit Funds Clause,

- The use of additional language to provide greater clarity, and

- Housekeeping and formatting updates.

The revised Standard Forms and new clause are now available on CREA WEBForms®.

Prior to the release, BCREA incorporated launch process safeguards, developed a communication plan for post-launch communications, reviewed current practices for updates, and tested for quality assurance with CREA’s WEBForms® team.

BCREA extends a big thank you to all the volunteers.

Launch Package

To help prepare REALTORS® and managing brokers integrate the new and revised Standard Forms into their practice, BCREA’s Launch Package includes watermarked versions of the revised forms highlighting the changes, guides, and a summary of the revisions.

Standard Forms Toolkits and Professional Development Courses

In addition to the launch, we’ve updated the Standard Forms Toolkits page and are working with our Instructors to update our Professional Development courses on CREA’s Learning Hub (login required).

If you have form or clause-related questions, email us at [email protected].

If you have questions about CREA’s WEBForms® or require support, please email CREA at [email protected].

2023 Throne Speech Outlines BC Government’s Housing Priorities

On February 6, 2023, Lieutenant Governor Janet Austin opened the fourth session of the 42nd parliament with a Throne Speech outlining Premier Eby’s governmental priorities.

While vague in specific policy deliverables, the Throne Speech outlined several broad initiatives directly impacting BC’s real estate sector.

Increasing Housing Supply

Budget 2023, which is set to be tabled on February 28, 2023, is promised to make record-level investments in housing for middle-class families. Pointing to investment and speculation as primary causes of rising housing costs, the government plans to invest in increased housing supply and services near transit hubs province-wide.

The provincial government also intends to launch a refreshed housing strategy and work with local governments and stakeholders to ensure this strategy results in more affordable homes for middle-class families, seniors, and those with the greatest need. The fall session will introduce laws to turn this strategy into new affordable housing.

Throughout the above-noted consultation process, BCREA is committed to advocating on behalf of BC REALTORS® and ensuring the voice of REALTORS® is heard loud and clear.

Anti-money Laundering

The Throne Speech reiterated the BC government’s commitment to supporting “people who work hard and play by the rules.” It announced that legislation will be introduced to crack down on money laundering. This legislation will likely be inspired by the Commission of Inquiry into Money Laundering in BC’s Final Report.

The government promises that this year’s multi‑billion-dollar surplus will be used to support British Columbians “now and for the long term,” so we can expect many new initiatives from the BC government in the coming year.

We understand the importance of staying informed and educated on policy matters that directly impact BC REALTORS®, and we are committed to keeping you informed on the latest policy developments.

As the new provincial government rolls out these new initiatives, we are dedicated to staying at the forefront of these changes and providing REALTORS® with policy updates.

Please refer to the full Throne Speech here for more information on Premier Eby’s key governmental priorities.

2024 BC Property Assessments

The 2024 BC Property Assessments are now available online through BC Assessment, and homeowners can now check theirs on the website and expect to receive their notices in the mail by the end of January 2024.

REALTORS® are often a valuable source of information for both buyers and sellers in helping them understand tax assessments and how they are used to calculate property taxes.

"Most homeowners around the province can generally expect about a -5 or +5 per cent rise in assessment values when they receive their notices in early January,” says BC Assessment assessor Bryan Murao. “Most homeowners can expect only modest changes in the range of -5% to +5%. These assessment changes are notably less than previous years.”

It is important to note that an increase in a property's assessment value does not necessarily mean an increase in property taxes for homeowners. In most cases, property taxes are only affected if a property's value is above the average value change for the community.

If a property owner is still concerned about their assessment after speaking to a BC Assesment appraiser, they may submit a Notice of Complaint (Appeal) by January 31st, for an independent review by a Property Assessment Review Panel.

For more information about assessments and trends in your area visit BC Assessment.

Managed Forest Land

BC Assessment has also issued an Important Notice to Purchasers of Private Managed Forest Land to make them aware of two aspects of tax law that have caused significant concerns for some purchasers:

- Purchasers of managed forest land may be responsible for paying taxes on timber previously harvested by the Vendor; and,

- Purchasers of managed forest land may be responsible for paying exit fees to the Managed Forest Council if the property is removed from managed forest class.

Prospective purchasers of privately managed forest land are advised to inquire about previous timber harvesting and its potential property tax implications. Exit fees may be incurred if the property is removed from managed forest land class before 15 years of enrollment.

For more information, visit the Managed Forest Council website or contact BC Assessment at [email protected] or call 1-866-valueBC (825-8322).

2025 BC Property Assessments

The 2025 BC Property Assessments are now available online through BC Assessment, and homeowners can now check theirs on the website and expect to receive their notices in the mail by the end of January 2025.

REALTORS® are often a valuable source of information for both buyers and sellers in helping them understand tax assessments and how they are used to calculate property taxes.

"Across the Lower Mainland and throughout BC, the overall housing market has generally stabilized in value for a second consecutive year," says BC Assessment Assessor Bryan Murao. "Most homeowners can expect only modest assessment changes in the range of -5 to +5 per cent."

For the Lower Mainland region, overall assessments have generally remained flat from about $2 trillion in 2024 to $2.01 trillion this year. Almost $27 billion of the region's updated assessments are from new construction, subdivisions, and property rezoning. The Lower Mainland region includes all of Greater Vancouver, the Fraser Valley, the Sea to Sky area, and the Sunshine Coast.

It is important to note that an increase in a property's assessment value does not necessarily mean an increase in property taxes for homeowners. In most cases, property taxes are only affected if a property's value is above the average value change for the community.

If a property owner is still concerned about their assessment after speaking to a BC Assessment appraiser, they may submit a Notice of Complaint (Appeal)Notice of Complaint (Appeal) by January 31, for an independent review by a Property Assessment Review Panel.

For more information about assessments and trends in your area visit BC Assessment.

2025 Begins With Strong Sales and Listings Activity

For the complete news release, including detailed statistics, click here.

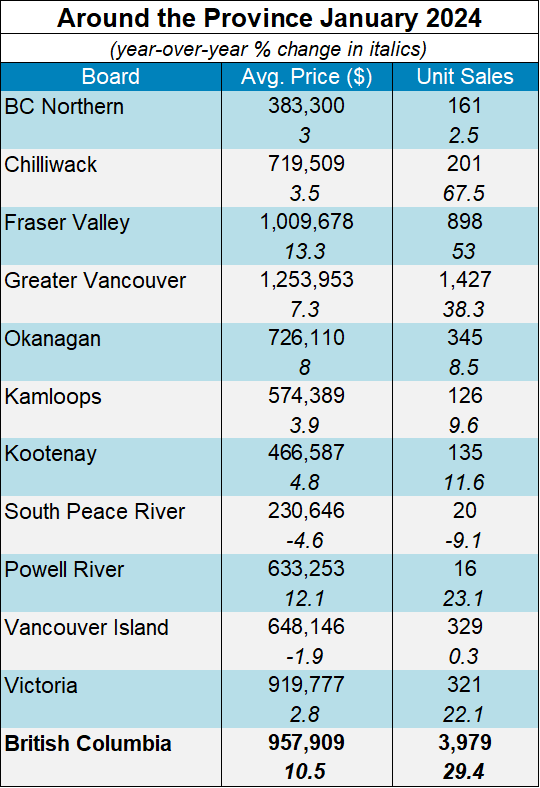

Vancouver, BC – February 13, 2025. The British Columbia Real Estate Association (BCREA) reports that 4,221 residential unit sales were recorded in Multiple Listing Service® (MLS®) Systems in January 2025, up 6.4 per cent from January 2024. The average MLS® residential price in BC in January 2025 was down 1.0 per cent at $949,560 compared to $959,191 in January 2024.